Mihir Torsekar

(202) 205-3350

Mihir.Torsekar@usitc.gov

For much of the past 20 years, U.S. manufacturing supply chains have been shaped by the relocation of labor-intensive elements of production to countries with low labor costs, supported in part by reduced duties on manufactured goods.[1] This has been reflected in the dependence of leading U.S. manufacturing sectors on imports of “intermediate goods” (manufactured parts or components) to make their products. Although U.S. imports of these goods contracted sharply during the 2007–09 global recession, since then they have rebounded in key manufacturing sectors, suggesting a continuation of the “offshoring” supply chain strategy already prevailing pre-recession. This chapter explores that relationship across the three manufacturing sectors—electronic products, machinery, and transportation—most heavily involved in intermediate goods trade.

Introduction

U.S. manufacturing supply chains have transformed over the past 20 years, owing to the relocation of some labor-intensive tasks—including parts and components manufacturing—to countries associated with low labor costs. This globalization of supply chains, better known as “offshoring,” tends to rely on the production of manufactured goods (most of which are intermediate inputs) abroad. The intermediate inputs are commonly manufactured by either a foreign affiliate or an independent supplier and are then imported back to the United States for final assembly.[2] As global manufacturing has become increasingly distributed across various countries, the volume of trade in intermediate goods has emerged as an important metric: it helps analysts both to better understand international trade flows and to discern the competitiveness of a country’s manufacturing sector.[3]

In the years since the end of the 2007–09 global recession, the share of imported intermediate inputs in the total intermediates used has grown substantially across the leading U.S. manufacturing sectors covered in the annual Trade Shifts report. This trend reflects a post-recession resumption of sourcing intermediate inputs from abroad that has persisted through 2016 (the final year for which these data are available).[4]

This chapter evaluates the data supporting offshoring trends by looking at three sectors closely associated with the intermediate goods trade: electronic products, transportation, and machinery.[5] It is divided into four sections. The first section discusses intermediate goods in greater depth and includes specific examples from each of the three sectors under review. Section 2 summarizes the overall trend in supply chain fragmentation and gives a broad overview of the United States’ largest suppliers of intermediate goods. Section 3 reviews the post-recession rebound of intermediate goods imports and presents trends in U.S. parent companies’ imports of these goods from their foreign affiliates by sector. The final section briefly discusses possible future trends in U.S. firms’ use of imported intermediate goods.

What Are Intermediate Goods?

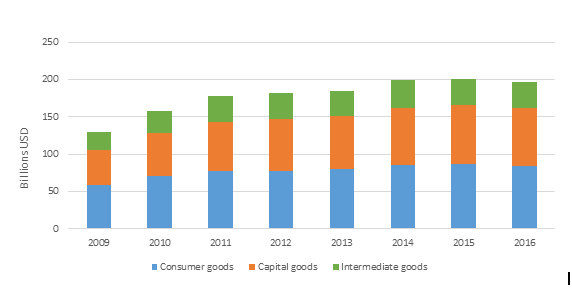

The goods covered by trade statistics can be subdivided into three broad categories: intermediate goods (parts or components that are embedded in final goods);[6] capital goods (fixed inputs that assist in the production of other goods); and consumption (or final) goods. In the years since the end of the 2009 global recession, the value of U.S. imports in all three categories have risen, with intermediate goods registering the second-fastest growth rate behind capital goods. While imports of capital goods grew 65 percent to $77.6 billion, imports of intermediate goods grew 48 percent to $34.7 billion (figure ST.1).

Figure ST.1 U.S. global imports of intermediate goods, capital goods, and goods for consumption have all increased since the end of the 2009 global recession (billion $).

Source: Compiled by USITC from World Integrated Trade Solution (WITS, World Bank), “U.S. Import of Consumer Goods, Capital Goods, and Intermediate Goods” (accessed May 12, 2018).

The three sectors discussed in this chapter are notable for their reliance on imports of intermediate goods. For example, one study found that in recent years, the electronics and transportation industries alone led all other industries combined in intermediate goods trade.[7] This is largely due to the types of components that are needed to manufacture finished goods in these industries. For example, the electronic products industry relies on integrated circuits, semiconductors, and microprocessors to produce finished products, which range from navigational equipment to computers and

smartphones.[8] The machinery industry employs various metals, plastics, and rubber to produce capital equipment for use in industrial applications, such as transmitting and distributing electric power, and in construction, agriculture, and semiconductor production.[9] Finally, the transportation sector—dominated by the automotive industry—uses many of the components listed in the two examples above (semiconductors, metals, plastics, etc.), but includes other inputs as well, such as fabrics and leather.

Largest U.S. Suppliers of Intermediate Goods

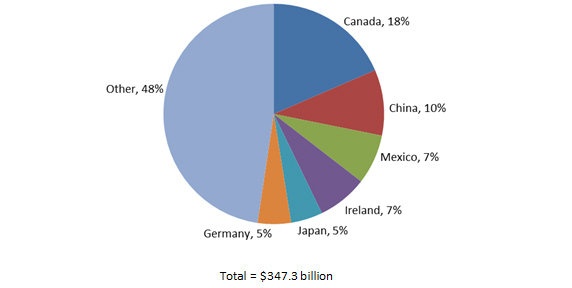

In 2016, the largest suppliers of intermediate goods to the United States were Canada, China, Mexico, and Ireland (figure ST.2). Canada and Mexico’s nearness to the United States (which reduces transportation costs) and membership in the North American Free Trade Agreement, or NAFTA (which grants duty-free access to member countries), has translated into their status as leading providers of intermediate goods to the United States.[10] China’s role as the United States’ second-largest supplier of components and parts reflects its predominance as a manufacturer of low-cost goods during much of the past two decades.[11] Finally, Ireland’s relatively low corporate tax rates and various tax incentives have drawn robust U.S. foreign direct investment (FDI) amounting to $277 billion over the past two decades by leading U.S. multinationals, outpacing that of any other country.[12] Much of what Ireland supplies to the United States reflects intra-firm trade between U.S.-based firms (e.g., Intel, Boston Scientific, Hewlett-Packard, Johnson & Johnson, etc.) and their Irish affiliates.

Figure ST.2 The three largest foreign sources of intermediate inputs to the United States’ market, by value, in 2016 were Canada, China, and Mexico, respectively.

Source: Compiled by USITC from WITS database, “U.S. Import of Consumer Goods, Capital Goods, and Intermediate Goods” (accessed May 12, 2018).

Increased Offshoring Post-recession

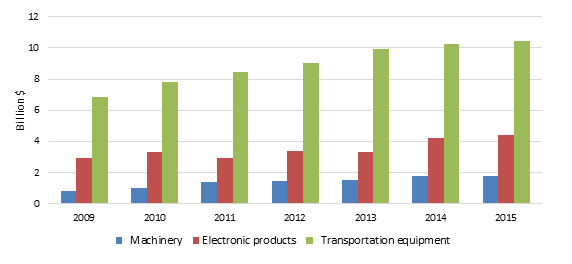

The severity of the 2007–09 recession is reflected in the fact that imports of intermediate goods for the three manufacturing sectors discussed in this chapter collectively declined by 52 percent (to $12.8 billion) during that time.[13] However, in the years since that contraction ended, growth of intermediate goods imports resumed for all three sectors under review, combining to reach $231 billion[14] by 2016. At the same time, imported intermediates as a share of total intermediates used in these three sectors rose at a steady pace throughout 2009–16, increasing by an average of five percentage points across these sectors (table ST.1). Further, imports by U.S. firms from their foreign affiliates[15] steadily increased during 2009–15 (figure 3). There were several reasons for these offshoring trends, including growing consumer demand for final goods, which buoyed demand for parts. This point is discussed in greater detail below.

Table ST.1 Imported intermediate goods (million $), total intermediate use (million $), and imported intermediates as a share of total intermediates used for the electronic products, machinery, and transportation equipment sectors, 2009–16.[16]

| Electronic Products and Computers | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 |

|---|---|---|---|---|---|---|---|---|

| Imported intermediate | 24,533 | 24,945 | 26,098 | 28,763 | 28,566 | 29,179 | 25,898 | 27,697 |

| Total intermediate use | 124,508 | 119,703 | 127,462 | 122,478 | 117,790 | 112,693 | 103,424 | 112,909 |

|

Imported intermediate/

Total intermediate use

|

20% | 21% | 20% | 23% | 24% | 26% | 25% | 25% |

| Machinery | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 |

| Imported intermediate | 27,557 | 35,060 | 44,888 | 54,218 | 50,748 | 54,970 | 48,924 | 44,096 |

| Total intermediate use | 168,868 | 193,977 | 228,872 | 264,056 | 249,814 | 260,263 | 234,730 | 222,622 |

|

Imported intermediate/

Total intermediate use

|

16% | 18% | 20% | 21% | 20% | 21% | 21% | 20% |

| Transportation | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 |

| Imported intermediate | 75,697 | 98,257 | 116,702 | 128,269 | 138,134 | 160,365 | 170,095 | 158,808 |

| Total intermediate use | 442,521 | 465,701 | 518,674 | 566,712 | 604,453 | 678,449 | 709,506 | 698,490 |

| Imported intermediate/Total intermediate use | 17% | 21% | 23% | 23% | 23% | 24% | 24% | 23% |

| All Other Manufacturing Sectors | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 |

| Imported intermediate | 890,076 | 1,075,317 | 1,260,962 | 1,263,754 | 1,234,369 | 1,257,238 | 1,081,155 | 1,046,142 |

| Total intermediate use | 9,502,602 | 10,349,761 | 11,143,038 | 11,554,745 | 11,937,617 | 12,554,990 | 12,263,065 | 12,426,428 |

| Imported intermediate/Total intermediate use | 9% | 10% | 11% | 11% | 10% | 10% | 9% | 8% |

Source: Compiled by USITC from Industry Economic Accounts (IEAs) and the Bureau of Economic Analysis (BEA).

Note: The BEA refers to the “electronic products” sector as “electronic products and computers” sector, and to the “transportation equipment” sector as simply “transportation.”

Figure ST.3 Imports by U.S.-based firms from their total global foreign affiliates grew by value for each of the three manufacturing sectors covered in this chapter during 2009–15 (billion $).

Source: Compiled by USITC from USDOC, BEA, “Data on Activities of Multinational Enterprises” (accessed April 3, 2018). Note: Data were not available beyond 2015.

In recent years, U.S. intermediate imports within the electronic products and equipment sector have increasingly been composed of semiconductor components. Eager to cut production costs and to produce goods closer to consumers in growing markets outside the United States, nearly all U.S.-based firms in the sector—integrated-device manufacturers (IDMs), “fabless” companies (i.e. semiconductor companies that specialize in design), and foundries (semiconductor manufacturers with no design capabilities)—have offshored semiconductor production since the end of the recession.[17] For example, U.S.-based imports from foreign affiliates associated with the manufacturing of semiconductors and other electronic components increased by $2.8 billion (24 percent) to $14.3 billion from 2009 to 2015.[18] Most of the imported intermediate goods for semiconductors have originated in Taiwan, where investment has been especially strong. However, Malaysia has also emerged as an important destination for offshored U.S. semiconductor processing, in addition to completing much of the final assembly for these products.

For the machinery sector, post-recession offshoring was significant in the category of investment that includes semiconductor manufacturing equipment and appliance manufacturing. Intra-firm imports within this category increased by a combined 157 percent to $6.3 billion in 2015.[19] In recent years, U.S. manufacturers have invested heavily in overseas production of components used to produce semiconductor manufacturing equipment, especially in the front-end segment of production (e.g., fab equipment and wafer manufacturing), the assembly and packaging equipment segments, and semiconductor testing equipment.[20] For example, U.S.-headquartered Intel Corporation increased such investments by $2.4 billion (25 percent) to $12.0 billion during 2016–17.[21] These investments have been stimulated by expanding markets for 3D NAND flash (a type of memory chip) and dominated by investment in advanced processing

technologies.[22] With respect to appliance manufacturing, price competition within the U.S. market has led to these firms to relocate production facilities for completed appliances and appliance parts to countries with lower labor costs, such as Mexico.[23]

Within the transportation sector, offshoring activity was led by the automotive subsector. U.S.-based firms within this category increased their imports from foreign affiliates by $35.7 billion (62 percent) during 2009–15 to $92.8 billion.[24] Robust demand for auto parts during this period in part reflected rebounding consumer demand for passenger vehicles; the number of total motor vehicle assemblies in the United States rose in each consecutive year during 2010–16, a nearly unprecedented period of growth for the auto industry.[25] At the same time, newly introduced industry standards on safety and technology have generated demand for parts ranging from microprocessors to sensors and from ignition switches to airbags. Further, parts demand has reflected the growing number of new car models available in the United States; as of 2017 there were 265 models available in the U.S., up from 211 in 2000.[26] It should be noted that this growth in imports of auto parts has not been consistent throughout the period. For example, U.S. imports of motor vehicle parts experienced a larger decrease (0.8 percent to $81.5 billion) than any other category of transportation equipment in 2017.[27]

Conclusion

As U.S. supply chains have become increasingly fragmented, imports of intermediate goods have played an important role in domestic manufacturing. After contracting substantially during the 2007–09 recession, intermediate goods imports, and the share of imported intermediate goods as a proportion of total intermediate goods used, has rebounded for the electronic products, machinery, and transportation equipment sectors in the United States. At the same time, imports by U.S.-based firms within these sectors from their foreign affiliates has also expanded. Taken in sum, these trends suggest the continuation of the offshoring strategy that U.S. firms have been pursuing since the mid-1990s.[28]

However, whether this post-recession offshoring trend will endure is uncertain. As new technologies (additive manufacturing, advanced robotics, artificial intelligence, etc.) foster supply chain innovations and yield production efficiencies, there is some speculation that the U.S. manufacturing sector may become less reliant on imported components. This claim is rooted in the assumption that factors such as low labor costs[29]—which have traditionally fueled offshoring—may be displaced by other considerations, such as improved time to market and reduced transportation costs. For example, various surveys of U.S. manufacturing firms reveal an emerging preference for shortening supply chains by increasing domestic production and adopting automated technologies.[30] While these technologies have not yet achieved widespread adoption, they may do so in the near future.

[1] UNIDO, Mapping Global Value Chains, 2011.

[2] The production of consumer goods is also offshored, but not as much as intermediate goods. When a good produced by a foreign affiliate is imported to its U.S.-based company, the transaction is referred to as intra-firm trade. Oldenski, “Reshoring by U.S. Firms,” September 2015.

[3] For example, imports of lower-cost intermediate goods can raise productivity while improving export competitiveness (due to lower production costs). Amiti, Freund, and Bodine-Smith, “Why Renegotiating NAFTA Could Disrupt Supply Chains,” April 18, 2017; OECD, “How Imports Improve Productivity and Competitiveness,” May 2010; OECD, “Imports: Improving Productivity and Competitiveness,” 2018.

[4] Data presented on intra-firm trade were available only up to 2015.

[5] UNIDO, Mapping Global Value Chains, 2011. Collectively, these three sectors accounted for nearly half of total trade for the United States in 2017, which includes all three categories of goods.

[6] Though not the focus of this chapter, intermediate inputs can also be services. For example, a consulting firm’s services offered to an electronic products company would be considered an intermediate input in the manufacturing of the final good.

[7] UNIDO, Mapping Global Value Chains, 2011.

[8] Diagne, “Made in America: Computer and Electronic Products,” 2012.

[9] Nicholson, “Made in America: Machinery,” 2012.

[10] Amiti, “Why Renegotiating NAFTA Could Disrupt Supply Chains,” April 18, 2017. Due to the frequency with which intermediate goods are traded—with value being contributed at each destination—these products are especially sensitive to tariffs and other trade costs. This explains why intermediate goods are most commonly traded among partners in regional trade agreements. OECD, “How Imports Improve Productivity and Competitiveness,” May 2010.

[11] From 1990 to 2015, Asia—led by China—led the world in global production, as measured by Asia’s percentage share of value-added manufacturing. Its shares grew from 24 percent to 45 percent during this period. Rose and Reeves, “Rethinking Your Supply Chain,” March 22, 2017.

[12] McDonald, “700 U.S. Companies Now Located in Ireland,” March 5, 2015.

[13] This decline eclipsed that observed for the entire manufacturing sector, U.S. imports of which fell by 32 percent to $50.3 billion.

[14] This figure was determined by adding total imported intermediates for electronic products and computers ($27,697,000,000), machinery ($44,096,000,000) and transportation ($158,808,000,000) for 2016.

[15] As previously discussed, these intra-firm transactions can be seen as a proxy for offshoring, because they reflect the goods (most of which are intermediate inputs) that are produced by U.S.-owned affiliates and then exported to the United States for final assembly. Oldenski, “Reshoring by U.S. Firms,” September 2015.

[16] For purposes of this figure, “imported intermediates” is defined as the total value of the imports of foreign-produced intermediate goods for U.S. final production. “Total intermediate use” is the combination of intermediate goods imported into the United States and U.S. produced-intermediate goods consumed for purposes of U.S. production into final goods (this does not include U.S.-produced intermediate goods which are then exported). Imported intermediates/total intermediate use is the ratio of U.S.-imported intermediate goods for U.S. production to imported plus domestically produced intermediate goods for U.S. production.

[17] VerWey, “Global Value Chains: Explaining U.S. Bilateral Trade Deficits in Semiconductors,” March 2018.

[18] USDOC, BEA, “Data on Activities of Multinational Enterprises” (accessed April 3, 2018).

[19] USDOC, BEA, “Data on Activities of Multinational Enterprises” (accessed April 3, 2018).

[20] SEMI, “$55.9 Billion Semiconductor Equipment Forecast,” December 12, 2017.

[21] Statista, “Leading Semiconductor Chip Manufacturers,” March 2017.

[22] Statista, “Leading Semiconductor Chip Manufacturers,” March 2017.

[23] IBISWorld, “Vacuum, Fan, and Small Household Appliance Manufacturing,” February 28, 2018.

[24] USDOC, BEA, “Data on Activities of Multinational Enterprises” (accessed April 3, 2018).

[25] Wood, “Demand for Automotive Parts to See Decline,” January 30, 2018.

[26] Gifford, “Car-parts Makers Strain to Keep Up,” February 23, 2015.

[27] For further information, please refer to the “Transportation Equipment” section of this report.

[28] Rose and Reeves, “Rethinking Your Supply Chain,” March 22, 2017.

[29] With the rise of wage rates in China—now at five times the level reported in 2005—the labor cost advantages associated with offshoring there have eroded. Deloitte, Global Manufacturing Competitiveness Index 2016, 2017.

[30] For example, BCG found that nearly 80 percent of the U.S. firms they surveyed in 2015 that pursued a localization strategy did so in order to shorten their supply chain; 70 percent to “reduce shipping costs”; and 64 percent to be “closer to [U.S.] customers.” Moreover, a 2014 UPS survey of U.S. firms in advanced technology sectors found that 35 percent of their respondents planned on relocating parts of their supply chain closer to the points of consumption—up 25 percent from 2010, when the same question was also posed. BCG, “Reshoring of Manufacturing,” December 10, 2015; UPS, “Change in the (Supply) Chain Survey,” November 2015.

Bibliography

Amiti, Mary, Caroline Freund, and Tyler Bodine-Smith. “Why Renegotiating NAFTA Could Disrupt Supply Chains,” April 18, 2017. https://piie.com/blogs/trade-investment-policy-watch/why-renegotiating-nafta-could-disrupt-supply-chains.

Boston Consulting Group (BCG). “Reshoring of Manufacturing to the U.S. Gains Momentum,” December 10, 2015. https://www.bcgperspectives.com/content/articles/.

Diagne, Adji Fatou. “Made in America: Computer and Electronic Products.” U.S. Department of Commerce. Economics and Statistics Administration, 2012. http://www.esa.doc.gov/sites/default/files/made-in-america-computer-and-electronic-products.pdf.

Deloitte Touche Tohmatsu (Deloitte). “2016 Global Manufacturing Competitiveness Index.” https://www2.deloitte.com/global/en/pages/manufacturing/articles/global-manufacturing-competitiveness-index.html (accessed April 6, 2018).

Baccini, Leonardo, Andreas Dür, and Manfred Elsig. “The Design of International Trade Agreements: Introducing a New Dataset.” Paper prepared for presentation at the ISA Annual Conference in San Francisco, April 3–6, 2013. https://www.designoftradeagreements.org/media/filer_public/bc/16/bc16bb53-a12e-4439-b93d-49370ad54d41/depth_flexibility_and_international_cooperation_-_the_politics_of_trade_agreement_design.pdf.

Gifford, Daron. “Car Parts Makers Strain to Keep Up with Technology Advancements.” MarketWatch, February 23, 2015. https://www.marketwatch.com/story/car-parts-makers-strain-to-keep-up-with-technology-advancements-2015-02-23.

Haugh, David, Alexandre Kopoin, Elena Rusticelli, David Turner, and Richard Dutu. Cardiac Arrest or Dizzy Spell: Why Is World Trade So Weak and What Can Policy Do about It? Organisation of Economic Co-operation and Development (OECD). Policy Paper No. 18, September 2016. http://www.oecd-ilibrary.org/economics/cardiac-arrest-or-dizzy-spell_5jlr2h45q532-en.

IBIS World. “Vacuum, Fan, and Small Household Appliance Manufacturing,” February 28, 2018. https://www.ibisworld.com/industry-trends/market-research-reports/manufacturing/electrical-equipment-appliance-component/vacuum-fan-small-household-appliance-manufacturing.html.

IBIS World. International Monetary Fund (IMF). World Economic Outlook: Subdued Demand; Symptoms and Remedies, October 2016. https://www.imf.org/en/Publications/WEO/Issues/2016/12/31/Subdued-Demand-Symptoms-and-Remedies.

McDonald, Henry. “700 U.S. Companies Now Located in Ireland as Direct Investment Soars.” Guardian, March 5, 2015. https://www.theguardian.com/world/2015/mar/05/ireland-attracts-soaring-level-of-us-investment.

Nicholson, Jessica R. “Made in America: Machinery.” U.S. Department of Commerce. Economics and Statistics Administration, 2012. http://www.esa.doc.gov/sites/default/files/machineryindustryprofile_0.pdf.

Organisation for Economic Co-operation and Development (OECD). “How Imports Improve Productivity and Competitiveness,” May 2010. https://www.oecd.org/trade/45293596.pdf.

Organisation for Economic Co-operation and Development (OECD). “Imports: Improving Productivity and Competitiveness,” 2018. http://www.oecd.org/trade/importsimprovingproductivityandcompetitiveness.htm.

Oldenski, Lindsay. “Reshoring by U.S. Firms: What Do the Data Say?” PowerPoint presentation. Peterson Institute for International Economics, September 2015. https://piie.com/publications/papers/oldenski20151007ppt.pdf.

Rose, Justin, and Martin Reeves. “Rethinking Your Supply Chain in an Era of Protectionism.” Harvard Business Review, March 22, 2017. https://hbr.org/2017/03/rethinking-your-supply-chain-in-an-era-of-protectionism.

SEMI. “$55.9 Billion Semiconductor Equipment Forecast—New Record with Korea on Top,” December 12, 2017. http://www.semi.org/en/559-billion-semiconductor-equipment-forecast-new-record-korea-top.

Statista. “Leading Semiconductor Chip Manufacturers,” March 2017.

United Nations Industrial Development Organization (UNIDO). “Mapping Global Value Chains: Intermediate Goods Trade and Structural Change in the World Economy” 2011. https://open.unido.org/api/documents/4811381/download/Mapping%20Global%20Value%20Chains%20-%20Intermediate%20Goods%20Trade%20and%20Structural%20Change%20in%20the%20World%20Economy.

United Parcel Service (UPS). “Change in the (Supply) Chain Survey,” November 2015. https://www.pressroom.ups.com/assets/pdf/pressroom/fact%20sheet/2015_UPS_CITC_executive%20summary.pdf.

United Parcel Service (UPS). “Eighth UPS Pain in the Chain Survey: Survey Snapshot,” 2015. https://www.ups.com/media/en/UPS-PITC-Executive-Summary-North-America.pdf.

U.S. Department of Commerce (USDOC). Bureau of Economic Analysis (BEA). Input-Output Accounts Data. https://www.bea.gov/industry/io_annual.htm (accessed July 6, 2018).

U.S. Department of Commerce (USDOC). Bureau of Economic Analysis (BEA). “Data on Activities of Multinational Enterprises.” https://www.bea.gov/iTable/index_MNC.cfm (accessed April 3, 2018).

VerWey, John. “Global Value Chains: Explaining U.S. Bilateral Trade Deficits in Semiconductors.” U.S. International Trade Commission. Executive Briefing on Trade, March 2018.

Wood, Bill. “Demand for Automotive Parts to See Decline.” Plastics News, January 30, 2018. http://www.plasticsnews.com/article/20180130/NEWS/180139994/demand-for-automotive-parts-to-see-decline.

World Integrated Trade Solution (WITS). “U.S. Import of Consumer Goods, Capital Goods, and Intermediate Goods between 2009–16.” https://wits.worldbank.org/CountryProfile/en/Country/USA/StartYear/1995/EndYear/2016/TradeFlow/Import/Indicator/MPRT-TRD-VL/Partner/BY-COUNTRY/Product/UNCTAD-SoP2# (accessed May 12, 2018).

World Integrated Trade Solution (WITS). “U.S. Export of Consumer Goods, Capital Goods, and Intermediate Goods between 2009–16.” https://wits.worldbank.org/CountryProfile/en/Country/USA/StartYear/1995/EndYear/2016/TradeFlow/Import/Indicator/MPRT-TRD-VL/Partner/BY-COUNTRY/Product/UNCTAD-SoP2# (accessed May 12, 2018).