Authors: André Barbé (Energy Economist), Andrew David (International Trade Analyst), and Alan Fox (International Economist)

1. Overview1

The significant decline in crude petroleum2 prices during 2014–15 provided a modest benefit for the U.S. economy overall, due to consumer gains and declining values of imported crude petroleum and related goods.3 These benefits were spread unevenly, however, both geographically and in terms of industry sectors. On the one hand, the drop in crude petroleum prices led to a decline in various energy-related input prices for certain manufactured goods; on the other hand, it triggered lower investment in global crude petroleum production, for which the United States is a large supplier of machinery and equipment. Both these declines contributed to substantial reductions in the value of U.S. exports across a broad range of manufacturing sectors.4 Because domestic crude petroleum production had recently expanded in the United States, the decline in energy prices had a heavier negative impact on operations within the United States than in previous instances. At the same time, in some energy-consuming industries, declining prices masked a rise in export quantities that reflect growing industry competitiveness.

This chapter supplements the other sections of 2015 Trade Shifts by examining the impact of declining crude petroleum prices on the U.S. economy, with a discussion of specific sectoral impacts. The reasons for the downturn in prices are addressed first, followed by a description of the impacts on the U.S. economy, on major crude petroleum-exporting and ‑importing countries, and on specific U.S. industrial sectors related to crude petroleum production.

2. Background: The 2014–15 Crude Petroleum Price Drop

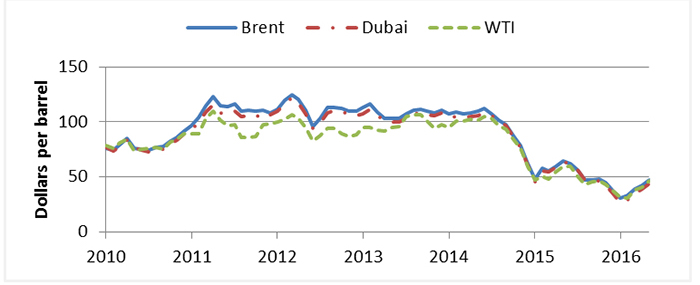

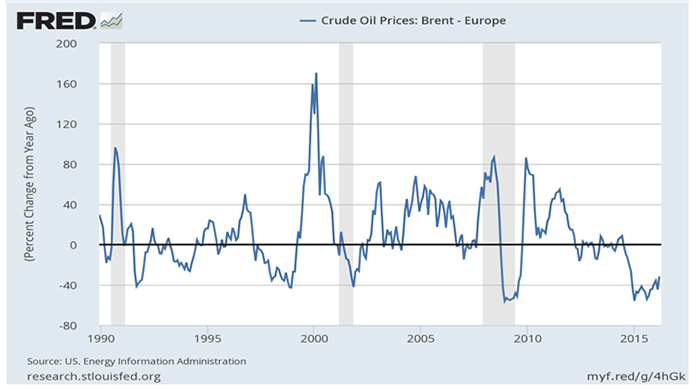

Crude petroleum spot prices fell by more than 60 percent between June 2014 and December 2015, after prices had hovered above $100 per barrel for the three previous years (figure ST.1).5 Over the last 25 years, sharp price increases and decreases have periodically affected crude markets (figure ST.2).6 As with all marketed goods, the price of crude petroleum is determined by its supply and demand.7 When there is a shock to either the supply of or the demand for crude petroleum, its price can change significantly.8 Because immediate and easy substitutes for crude petroleum and related products are not readily available to consumers, the quantities of crude petroleum supplied and consumed are relatively constant, despite significant changes to prices.9

Figure ST.1: Crude petroleum prices fell sharply starting in mid-2014

Source: World Bank Commodity Markets data (accessed July 6, 2016).

Notes: Brent, Dubai, and West Texas Intermediate (WTI) are major world benchmarks for the price of crude petroleum. See appendix table DT.ST.1 for the data table.

Figure ST.2: Over the last 25 years, sharp price increases and decreases have periodically affected crude markets

Source: Federal Reserve Bank of St. Louis, “Crude Oil Prices: Brent—Europe,” FRED Economic Data (accessed July 6, 2016)

Notes: Price of crude petroleum as measured by monthly Brent spot price FOB $/bbl. As noted on the FRED website, “Shaded areas indicate U.S. recessions.” The data for this graph can be downloaded at the website.

The current academic literature presents a number of competing explanations for the 2014–15 crude price drop. Among the factors considered in these explanations are changes in supply and demand, though there is no agreement in the literature on which factor (i.e., supply or demand) played a greater role. A particular area of disagreement is the role of supply decisions after the prices began to decline in July 2014.10 Arezki and Blanchard, Baffes et al., and the International Monetary Fund find that while both supply and demand were important, supply factors (in the aggregate) were the root cause of the recent crude price drop.11 The main changes in supply included increased production of crude petroleum from U.S. shale and the decision of the Organization of the Petroleum Exporting Countries (OPEC) not to lower production in response to falling prices.

However, not everyone agrees that supply played the primary role in the price drop. For example, Kilian, while recognizing that supply factors occurring before July 2014 (when prices began to decline) contributed to the price drop, finds that the data do not support a major role for the abovementioned supply factors that occurred after crude prices began to decline.12 Baumeister and Kilian have found that adverse demand shocks, such as a slowing Chinese demand and an unexpectedly weak global economy, accounted for a majority of the price drop.13

Two alternative explanations linked to both the supply of and the demand for crude petroleum are speculation by hedge funds or other financial agents, and currency exchange rates. However, the literature does not show that financial speculation was important. Baumeister and Kilian also make several arguments for skepticism regarding an exchange-rate-based explanation.14 (For a short discussion on natural gas pricing, see box ST.1.)

|

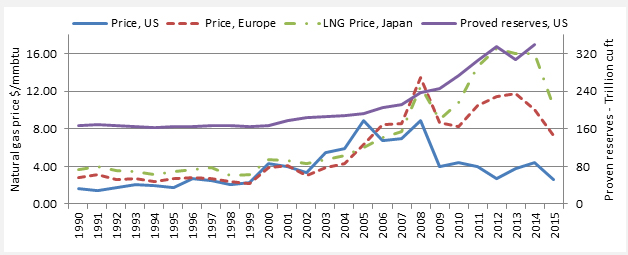

Box ST.1: Declining Natural Gas Prices Like the price of crude, natural gas prices fell during 2014–15 (see figure ST.3). However, natural gas is more costly to transport than crude petroleum, as it requires dedicated pipelines or must be transported after being liquefied. As a result, the price drop differed substantially by region. In particular, natural gas prices for industrial use fell by a little over 20 percent in the OECD on average, but by 40 percent in the United States.15 Crude petroleum and natural gas prices generally tracked one another, but with some regional differences.16 While the two prices are related, the relationship can shift dramatically.17 In the past eight years, the price of natural gas in the United States, Europe, and Asia diverged widely (figure ST.3).18 U.S. proven natural gas reserves nearly doubled from 2000 to 2014, contributing to the decline in U.S. natural gas prices. Figure ST.3: The prices of natural gas in the United States, Europe, and Asia diverged widely in the last eight years  Source: World Bank, Commodity Markets Data, 2016 (accessed July 6, 2016).Note: See appendix table DT.ST.3. |

3. Effects on the U.S. Macroeconomy

The estimated net effect of the decline in crude petroleum prices on the U.S. macroeconomy has been modestly positive.19 According to the Council of Economic Advisers (CEA) annual report, which provides a partial estimate of the effect of declining crude prices on real GDP, the direct effects alone accounted for real GDP growth of 0.1 percent in 2014 and 0.2 percent in 2015 (see a decomposition of GDP growth in table ST.1).20

Table ST.1: Estimated impact of crude petroleum price declines on GDP, 2014–15 (percent)

|

Growth

|

|||||||

|---|---|---|---|---|---|---|---|

| 2014 | 2015 | Cumulative level | |||||

| Total impact | 0.1 | 0.2 | 0.3 | ||||

| Contribution from: | |||||||

| Consumption (via imported-oil savings) | 0.1 | 0.5 | 0.6 | ||||

| Drilling and mining investment | 0.0 | -0.3 | -0.3 | ||||

Source: CEA, Annual Report of the Council, 2016, 55, table 2-i.

Declining energy prices give U.S. consumers more disposable income. The money saved on household energy expenditures can be used to boost other consumption, pay down debt or increase savings, or expand consumption of cheaper energy goods. Energy-intensive industries also benefit, as the cost of an important input to production declines. However, the sharp decline in prices depresses the energy-producing sectors in the U.S. economy, reducing profits, costing jobs, and curtailing investment in energy exploration. Since the United States is a net energy importer, lower energy prices can improve the U.S. trade deficit as spending on energy imports declines. This same fall in price, however, can reduce energy-exporting partners’ incomes and hence their demand for U.S. exports of goods and services. This decline in U.S. exports reduces improvement in the U.S. trade deficit.

3.1 Impact on U.S. Consumption

According to the CEA analysis, the price decline benefited U.S. consumers, with consumption benefits (via savings on imported oil) contributing 0.5 percent growth to GDP in 2015.21 While price declines for imported crude provide broad economic and consumer benefits, the GDP effects of declining prices for domestically produced and consumed crude petroleum roughly cancel out. Consumers benefit from lower prices, but the domestic industry experiences a roughly equal offsetting contraction from the price decline (table ST.2).22

Table ST 2: U.S. imports of crude petroleum: quantity and value

| Import quantity (million barrels) |

Quantity change from previous year (percent) |

Import value (billion dollars) |

Value change from previous year (percent) |

|

| 2013 | 2,821.5 | -9.6 | 273.8 | -13.3 |

| 2014 | 2,680.6 | -5.0 | 247.0 | -9.8 |

| 2015 | 2,682.9 | 0.1 | 126.1 | -49.0 |

Sources: U.S. Department of Energy, “U.S. Imports by Country of Origin” (accessed July 6, 2016); DataWeb/USDOC (accessed June 2016).

3.2 Impact on U.S. Energy Sector Investment

Crude petroleum price declines also contributed to lower U.S. investment in oil and gas production, which had a negative impact on GDP growth. As prices and profits in the domestic energy sector fell, so too did investment in oil and gas exploration and production. The number of U.S. oil rigs in operation, for example, dropped 63 percent from the September 2014 peak to December 2015.23 According to the CEA, lower investment in crude production translated into a 0.3 percent decline in GDP growth (table ST.1). The decline of investment in natural gas exploration, not addressed by the CEA analysis, also was likely to be contractionary for U.S. GDP. The negative effects of declining prices tend to be unevenly concentrated in U.S. states in which significant portions of the economy rely on the extraction of crude petroleum and natural gas (box ST.2).

|

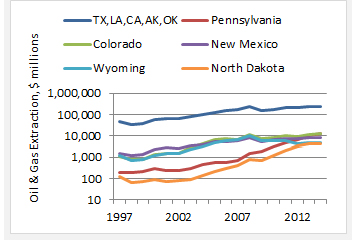

Box ST.2: The Crude Petroleum and Natural Gas Industry at the U.S. State Level27 The increase in crude petroleum and natural gas production over the past 20 years helps explain the different degrees of economic exposure to crude petroleum price shocks across the United States.28 Significant portions of the economy in the traditional top 5 producing states are tied to petroleum and gas production and, increasingly, the same is true for the next 5 producing states. The relatively concentrated nature of crude petroleum and natural gas production means that top producing states disproportionately face the adverse industry effects of these same low prices. The crude petroleum and natural gas production sector grew nationally at a compound annual growth rate of 10.5 percent over 1997–2014 (NAICS 211: oil and gas extraction), with the combined state GDP of the 5 traditional producers almost matching that rate at 9.9 percent.29 However, primarily due to shale-related production, crude petroleum and natural gas production grew at a much higher average rate in three states: Pennsylvania (28.9 percent), North Dakota (23.1 percent), and Colorado (16.1 percent) (figure ST.4). Pennsylvania’s production grew from a modest $197 million in 1997 to almost $13.3 billion by 2014, pushing petroleum and gas from 0.1 percent of Pennsylvania’s GDP to 2.0 percent by 2014. The industry is still a relatively minor part of the state’s economy, however, accounting for the second-lowest proportion of GDP among the top 10 producing states (table ST.3). North Dakota’s transformation has been far greater, with petroleum and gas rising from 0.8 percent of the state’s economy in 1997 to 7.4 percent in 2014. Colorado experienced an increase from 0.7 percent in 1997 to 4.2 percent in 2014. On a combined basis, the average for the top 10 producing states rose from 2.1 percent to 5.1 percent over this period, while the remaining 40 states saw almost no change.

|

4. Effects on the Global Economy

The decline in crude petroleum prices had a significant impact on the world economy in 2015, though the impacts varied by country. The fall in the price of crude petroleum generally shifts income from crude petroleum-exporting countries, which now sell their crude for less, to crude-importing countries, which pay less for the crude they buy. The overall impact on global GDP is not yet clear, as it depends on whether the price decline is supply or demand driven (which is still the subject of some debate, as noted above). For example, Kilian argues that the sharp increases in crude petroleum prices following 2003 did not cause a U.S. recession because it was driven by a sustained demand increase from a booming global economy, rather than crude supply disruptions or unexpected increases in precautionary demand.24 Several previous studies have estimated that a supply-driven crude petroleum price decline of about 50 percent would increase world GDP by around 0.7 percent.25 In particular, Arezki and Blanchard calculate that the 50 percent crude price decline in 2014 would increase world GDP by 0.7 percent if 60 percent of it were driven by expanding supply.26 The next two sections briefly review the impact on petroleum-exporting and -importing countries.

4.1 Crude-Exporting Countries

Worldwide, GDP growth rates for many (though not all) major crude petroleum exporters declined in 2015, driven in part by falling crude petroleum prices (table ST.4).30 Several empirical studies examined the impact of a price decline on exporters such as Canada, Russia, Algeria, Iran, Iraq, and Kuwait, among others. They found that these countries’ GDP could fall by 0.8 to 2.5 percent following just a 10 percent decline in the price of crude.31 A study by the Bank of Canada estimated that the Canadian GDP would fall by about 1 percent if the price of crude fell from $110 to between $50 and $70 per barrel (the price actually fell to $38).32 The analyses of Brazil and Russia in this year’s Trade Shifts report also highlight the negative impact of declining crude prices on these economies.33

Table ST.4: GDP growth rates of selected major crude petroleum exporters (percent change, year over year)

Country |

2011 | 2012 | 2013 | 2014 | 2015 |

| Canada | 3.1 | 1.7 | 2.2 | 2.5 | 1.2 |

| Russia | 4.3 | 3.5 | 1.3 | 0.7 | -3.7 |

| Saudi Arabia | 10.0 | 5.4 | 2.7 | 3.6 | 3.4 |

| Venezuela | 4.2 | 5.6 | 1.3 | -3.9a | -5.7a |

Source: IMF, World Economic Outlook Database, GDP, constant prices, percent change, 2016 (accessed May 25, 2016).

a Venezuela’s GDP growth rates in 2014 and 2015 are estimates by the IMF, World Economic Outlook Database (accessed May 25, 2016).

U.S. exports of goods to a number of major crude petroleum exporters fell, in large part due to reduced economic activity in these countries. For example, this was a major factor in the 34 percent fall in U.S. exports to Russia and the 25 percent decline in U.S. exports to Venezuela (table ST.5).34 While Canada’s GDP increased, albeit at a slower rate, in 2015, declining crude and natural gas prices and investment were a significant factor in the fall in U.S. exports to Canada. The effect of lower demand in these countries is discussed in the individual sectoral analyses and in the manufactured goods export section below.

Table ST.5: Annual growth in value of U.S. exports to major crude petroleum exporters (percent change, year over year)

Country |

2011 | 2012 | 2013 | 2014 | 2015 |

| Canada | 12.9 | 4.0 | 2.8 | 4.0 | -10.3 |

| Russia | 38.8 | 28.6 | 4.2 | -3.5 | -34.1 |

| Saudi Arabia | 21.0 | 29.0 | 5.6 | -1.3 | 5.5 |

| Venezuela | 16.3 | 41.5 | -24.6 | -15.3 | -25.3 |

Source: USITC DataWeb/USDOC (accessed July 7, 2016).

4.2 Impacts on Crude Importers

Crude importers may have benefited from the crude petroleum price declines in 2015, but in some instances the rate of GDP growth in major importing countries still slowed (e.g., China and South Korea; table ST.6) due to other economic factors.35 Major importers generally benefit from a decline in the price of crude petroleum, with research suggesting that a 10 percent reduction in the price of crude could increase an importing country’s GDP by 0.1 to 0.5 percent.36

Table ST.6: GDP growth rates of selected major crude petroleum importers (percent change, year over year)

Country |

2011 | 2012 | 2013 | 2014 | 2015 |

| China | 9.5 | 7.7 | 7.7 | 7.3 | 6.9 |

| India | 6.6 | 5.6 | 6.6 | 7.2 | 7.3 |

| Japan | -0.5 | 1.7 | 1.4 | 0.0 | 0.5 |

| South Korea | 3.7 | 2.3 | 2.9 | 3.3 | 2.6a |

Source: IMF, World Economic Outlook Database, GDP, constant prices, percent change, 2016 (accessed May 25, 2016).

a South Korea’s GDP growth rate in 2015 is an estimate by the IMF, World Economic Outlook Database (accessed May 25, 2016).

U.S. exports to major petroleum importing countries generally did not rise with declining crude petroleum prices (table ST.7). In part, this reflected the fact that other economic factors contributed to slower growth and less demand for imports from the United States.37 In addition, energy-related products (e.g., natural gas and components, and petroleum products) are a significant component of U.S. exports to some of these countries, and lower prices for these products contributed to lower export values.

Table ST.7: Annual growth in value of U.S. exports to selected major crude petroleum importers (percent change, year over year)

Country |

2011 | 2012 | 2013 | 2014 | 2015 |

| China | 13.3 | 6.1 | 10.2 | 1.5 | -6.1 |

| Japan | 8.8 | 6.3 | -6.8 | 2.5 | -6.6 |

| India | 11.9 | 2.6 | -1.3 | -1.4 | -0.2 |

| South Korea | 12.0 | -2.7 | -1.5 | 7.1 | -2.6 |

Source: USITC DataWeb/USDOC. (accessed July 7, 2016).

5. Impact on U.S. Manufactured Goods Trade

Declines in the prices of crude petroleum and natural gas had a significant impact on U.S. manufactured goods trade in 2015. The value of U.S. exports significantly declined in 2015, in large part due to lower crude and natural gas prices and investment. U.S. imports were also affected, but the oil- and gas-related import declines were largely offset by higher imports of consumer goods. This section provides an overview of several U.S. manufacturing sectors that were directly and indirectly affected by the declining price of crude petroleum.38 The sectoral and trade partner-specific discussions in this report provide more detail on the impact of declining energy prices and investments on trade in those sectors or with those trading partners.

5.1 U.S. Exports

The decline in crude petroleum and natural gas prices was a major driver of the fall in the value of U.S. manufactured goods exports in 2015. The lower prices affected exports in two ways:

- Lower prices contributed to a decline in capital expenditures abroad related to the production, transport, and refining of crude petroleum and natural gas. This led to lower U.S. exports (in both quantity and value) of goods such as oil and gas field equipment, pumps, and line pipe, casing, and tubing for oil and gas. These effects were spread broadly across a range of U.S. manufacturing industries, including many that are not typically characterized as suppliers to the energy sector.

- Lower feedstock prices for petroleum refinery products, organic chemicals, plastic resins, and other products contributed to a decline in the value—though not necessarily the quantity—of U.S. exports of these goods.

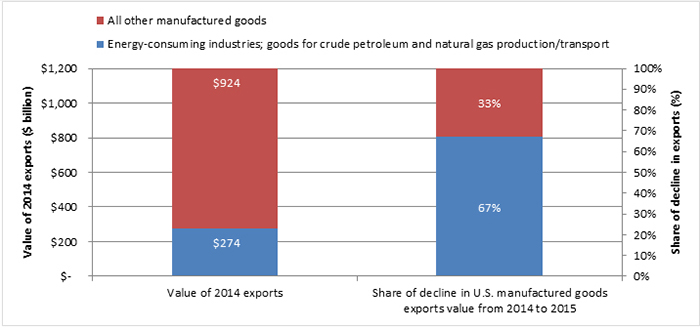

As a result, U.S. exports of products in major energy-consuming and -supplying industries, which accounted for only 23 percent of 2014 U.S. manufactured goods exports, accounted for 67 percent of the 2014–15 decline in manufactured goods exports. A broadly defined composite of “all other manufactured goods” accounted for (by definition) the remaining 33 percent of the decline in U.S. manufacturing goods exports (figure ST.5).

Figure ST.5: Despite accounting for only a quarter of 2014 manufactured goods exports, products closely related to petroleum production accounted for about two-thirds of the decline in durable goods exports between 2014 and 2015

Source: Compiled from official statistics of the U.S. Department of Commerce. These reflect all official revisions of previously published data up to June 2015 (accessed April 26, 2016).

Notes: Energy-consuming industries are those industries for which the cost of purchased fuels (according to the U.S. Census’s Annual Survey of Manufactures) accounted for 5 percent or more of value added. This captures most of the industries that also purchase fuels as feedstocks in the production process. However, it does not include asphalt shingle and coating materials manufacturing and cyclic crude and intermediates, so these were added in for the purpose of this analysis.

Goods for natural gas and crude petroleum production and transport include oil and gas field machinery and equipment, pumps, and other engine equipment. Iron and steel are already captured by the selection of the energy-consuming industries. This only includes a small share of the sectors affected by declining demand for crude petroleum and natural gas production and transport equipment, as will be discussed below. Data are classified by NAICS National Industry (6-digit) code.

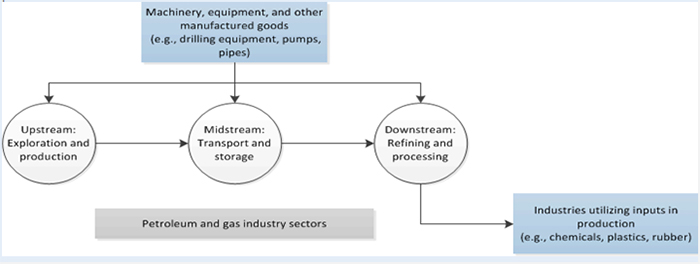

This section will focus on the impact of crude petroleum and natural gas prices on U.S. exports of manufactured goods.39 The discussion will focus on (1) exports of machinery, equipment, and other durable goods used to explore for, produce, transport, store, and refine crude petroleum and natural gas; and (2) exports by industries (e.g., chemical, plastics, synthetic rubber) that use natural gas and petroleum products as production inputs (figure ST.6).

Figure ST.6: These industries were significantly impacted by declines in crude petroleum and natural gas prices in 2014–15

Source: Compiled by USITC staff from PSG, “Defining Upstream Oil and Gas” (accessed July 8, 2016); EKT, “Upstream vs Downstream Oil and Gas” (accessed July 8, 2016); and STI Group, “What is Downstream?” (accessed July 8, 2016).

Note: Certain chemicals industries, synthetic rubber, etc., are often considered part of the downstream petroleum and gas industry. They are separated here for clarity of the products covered in this analysis.

5.1.1 Effects on Durable Goods Exports

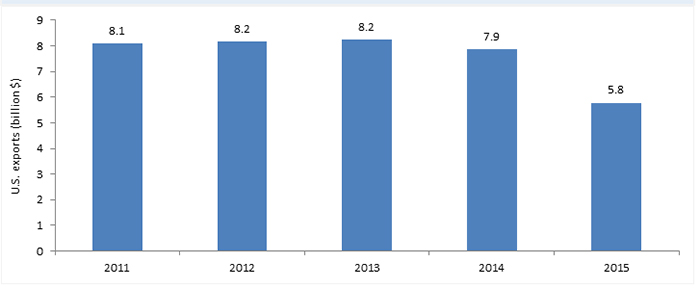

The decline in U.S. exports of durable goods40 during 2014–15 was driven, in part, by falling investment in global crude petroleum and natural gas production. Global revenues for oil field equipment companies were 30 percent lower in the third quarter of 2015 than in the third quarter of 2014, according to McKinsey. Bloomberg estimates that oil and gas capital expenditures declined 20 percent in 2015, including an almost 40 percent decline in upstream capital expenditures.41 Similarly, the number of active non-U.S. drilling rigs globally declined 35 percent from December 2014 to December 2015.42 This contributed to a 26 percent ($2.1 billion) decline in U.S. exports of oil and gas field machinery and equipment43 in 2015 (figure ST.7).44

Figure ST.7: The value of U.S. domestic exports of oil and gas field machinery and equipment significantly declined in 2015

Source: Compiled from official statistics of the U.S. Department of Commerce for the 2011–15 period. These reflect all official revisions of previously published data up to June 2015 (accessed April 26, 2016).

Note: U.S. exports in NAICS 333132, oil and gas field machinery and equipment manufacturing.

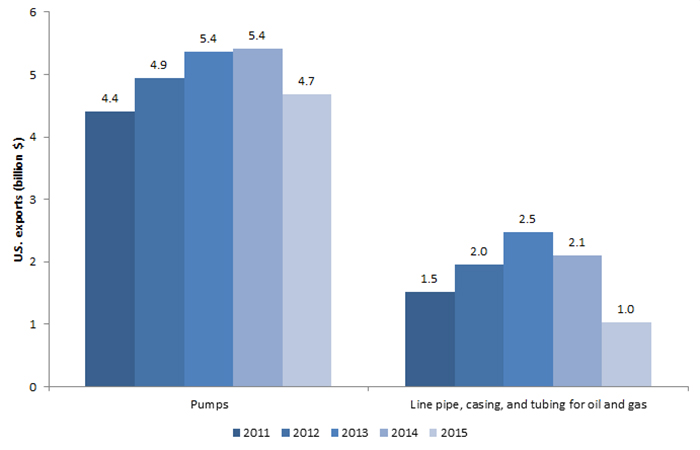

Declining investment in crude petroleum and natural gas also contributed to a downturn in exports in a range of other industries. U.S. pump exports declined by $738 million, largely driven by a decline in demand for pumps in the oil and gas industry (figure ST.8).45 U.S. exports of line pipe, casing, and tubing specifically classified for use related to oil and gas fell by 53 percent ($0.8 billion).46 A broader analysis of several countries in South America further illustrates that the decline in U.S. exports of durable goods to major petroleum companies in Argentina, Colombia, Ecuador, and Venezuela was spread across a range of products, with substantial reductions in exports of products like power generation equipment.47 Examining U.S. trade with India, exports of goods identified for use in oil wells, oil fields, and drilling and shipped to the port of Mumbai included a diverse range of products, such as valves and bearings. Exports of these goods to the port of Mumbai declined 33 percent during 2014–15.48

Figure ST.8: The decline in crude petroleum and natural gas prices and lower investment in production were key drivers of the decline in exports of products like pumps and line pipe, casing, and tubing (2014–15)

Source: USITC DataWeb/USDOC (accessed July 26, 2016).

Note: Includes all pump exports in NAICS 333911, and pipe, casing, and tubing in Harmonized System Codes (HS) 7304.11–29, 7305.11–20, 7306.11–29. See appendix table DT.ST.8.

5.1.2 Effect on Industries Using Petroleum- and Natural Gas-Related Inputs

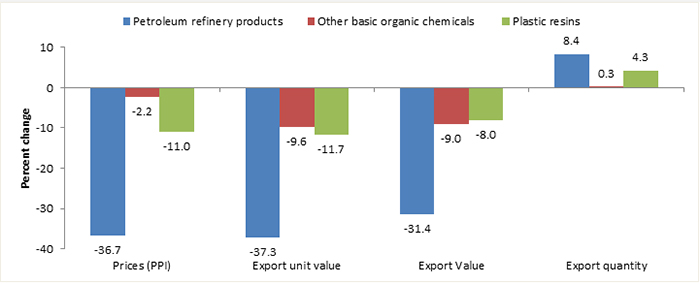

The decline in crude petroleum and natural gas prices also led to declines in the value of U.S. exports of many goods using these products as inputs. Three of the largest sectors in terms of the decline in the value of U.S. exports in 2015 used significant inputs from crude petroleum and natural gas production—petroleum refinery products, other basic organic chemicals, and plastic resins and materials.49 These manufacturing sectors recorded significant declines in the value of exports, but these declines were largely related to lower prices for these goods (resulting from lower input prices)—the quantity of exports in all of these sectors increased (figure ST.9).50 U.S. producers have become more competitive in products such as polyethylene.51 Price effects were not limited to these sectors, but were spread across a range of industries. For example, the 11 percent ($476 million) decline in the value of exports of synthetic rubber products was largely due to the 12 percent decline in prices as measured by the producer price index (PPI).52

Figure ST.9: The value of U.S. exports in many oil and gas consuming sectors declined, while the quantity of exports increased (2014–15)

Source: Compiled from official statistics of the U.S. Department of Commerce. These reflect all official revisions of previously published data up to June 2015 (accessed April 26–May 5, 2016); U.S. Department of Labor, Bureau of Labor Statistics, PPI databases, “Commodity Data” (accessed May 5, 2016).

Note: PPI = producer price index. Trade data are based on NAICS 324110 (petroleum refinery product), 325199 (all other basic organic chemicals), and 325211 (plastic materials and resins), and may not match trade data elsewhere in this report presented in terms of digests. Export units and export unit values for petroleum refinery products and other organic chemicals are based in the unit of quantity that accounted for the most trade in these products. PPI are based on the commodity data series. See appendix table DT.ST.9.

Price effects were less significant further downstream and likely had a smaller impact on U.S. exports. For example, despite the 11 percent decline in plastic resin prices, plastic products prices fell only 1 percent in 2015, and prices for some types of plastic products increased.53 Similarly, trends in export prices were mixed in 2015, with prices decreasing in only half the Harmonized System (HS) 6-digit subheadings for plastic products.54 However, if lower prices persist, they may have a heavier impact on the value of U.S. exports in 2016.55

5.2 U.S. Imports

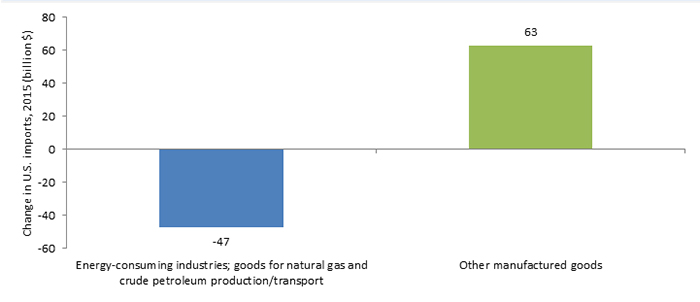

The total value of U.S. imports of manufactured goods remained relatively unchanged in 2015 compared to 2014.56 As with exports, there were significant declines in the value of imports in energy-consuming and ‑supplying industries (figure ST.10). This included declines in two types of imports: imports of machinery, equipment, and other durable goods used by the upstream and midstream energy industries, and imports by industries using natural gas and petroleum products as inputs into production.57 These declines were offset, however, by increases in U.S. imports of other products, such as autos, pharmaceuticals, and telecommunications apparatus.

Figure ST.10: The decline in imports by energy-consuming and -supplying industries was offset by an increase in imports of other manufactured goods

Source: Compiled from official statistics of the U.S. Department of Commerce. These reflect all official revisions of previously published data up to June 2015, https://dataweb.usitc.gov (accessed April 26, 2016).

Notes: Energy-consuming industries are those industries for which the cost of purchased fuels (according to the Annual Survey of Manufacturers) accounted for 5 percent or more of value added. This captures most of the industries that also purchase fuels as feedstocks in the production process. However, it does not include asphalt shingle and coating materials manufacturing and cyclic crude and intermediates, so these were added in for the purpose of this analysis. Goods for natural gas and crude petroleum production and transport include oil and gas field machinery and equipment, pumps, and other engine equipment. Iron and steel are already captured by the selection of the energy-consuming industries. This only includes a small share of the sectors affected by declining demand for crude petroleum and natural gas production and transport equipment, as will be discussed below. Data are by NAICS National Industry (6-digit) code.

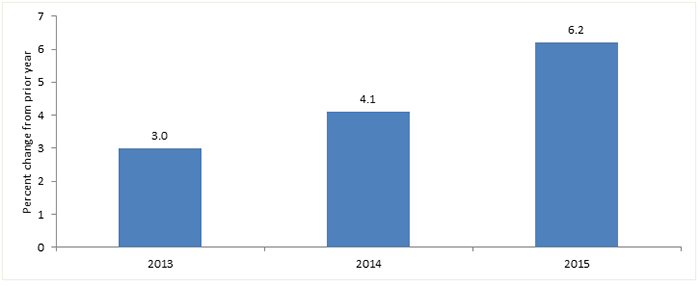

Imports of consumer goods,58 in particular, increased at a rapid pace in 2015, rising 6.1 percent (figure ST.11).59 This reflects (at least in part) increased U.S. consumption, some of which was related to a rise in consumer income due to lower prices for crude petroleum, as discussed above.60 Growth was distributed unevenly, however, as imports increased in 61 percent of HS 6-digit subheadings, and declined in 39 percent of these subheadings.61

Figure ST.11: Consumer goods imports increased at a rapid pace in 2015

Source: Compiled from official statistics of the U.S. Department of Commerce. These reflect all official revisions of previously published data up to June 2015 (accessed June 1, 2016).

Notes: The definition of consumer goods is based on the United Nations Conference on Trade and Development (UNCTAD) list of HS 6-digit subheadings, excluding goods in chapter 27 and any products that are not considered manufactured goods in the NAICS. Since this list is at the HS 6-digit level, it likely includes some products that are not typically considered consumer goods but are part of a broad subheading. For the list of goods, see the World Bank website, http://wits.worldbank.org/referencedata.html (accessed June 1, 2016).

6. Conclusion

According to the CEA, the impacts of the decline in crude petroleum prices on the overall U.S. economy appear to have been modest, amounting to 0.2 percent direct increase in U.S. GDP growth in 2015.62 The impacts on certain U.S. manufactured exports were substantial, and ranged from declines in exports of durable goods used in the production, transport, and refining of crude petroleum to declines in the value (though not necessarily the quantity) of exports by major energy-consuming industries. This reflects the fact that the U.S. economy is not only a major importer of energy goods, but also a major exporter.

The United States has increased production of crude petroleum and natural gas in the past few years, with corresponding increases in exports of related products. Therefore, declines in crude petroleum prices had an immediate impact on the value of U.S. exports, likely more so than in the earlier instances of price declines. Combined with other global economic headwinds discussed in this report (see the “Overall Economic Performance“ webpage), the crude petroleum price decline contributed to a large drop in the value of U.S. exports. Exports of goods in most sectors declined, even to trading partners that are major importers of crude petroleum and related products.

U.S. consumers and some industries, on the other hand, benefited from the declining crude petroleum and natural gas prices. In some energy-consuming industries, export volume increased (despite the overall decrease in export values), and low energy product input prices are making these industries more competitive globally. U.S. consumers also had more money available to spend, which is reflected in the large increase in U.S. imports of consumer goods in 2015.

The characteristics of the United States—as both a major exporter/producer and a major importer of energy products—means that the distribution of impacts from energy price declines were felt unevenly. In a number of producing states, such as Alaska, Wyoming, Texas, and Oklahoma, oil and gas extraction accounts for a large (and until recently growing) share of state GDP. Crude petroleum price declines are more likely to immediately impact industries and consumers in these states, and losses by producers of energy-related goods were deep and concentrated. Gains were distributed to sectors that benefit directly from lower input prices and to U.S. consumers, with net benefits particularly accruing to those states in which oil and gas extraction does not account for a substantial share of GDP.

1 In this chapter, “energy” is used to refer to petroleum and natural gas, and does not include other energy products (such as coal and renewable energy).

2 What is called “crude petroleum” (or “crude”) in this chapter is often called “crude oil” by other sources. To discuss crude petroleum pricing, the analysis in the “Energy and Related Products“ webpage of this report uses a weighted average global price of West Texas Intermediate (WTI) and Brent crude petroleum, while this chapter uses the monthly Brent spot price (as reported by the U.S. Department of Energy) to reflect the volatility of crude prices. Spot prices are a reasonable proxy for price paid. While financial instruments such as futures contracts and options contracts can shift the risk of price volatility within the economy, they do not materially change GDP.

3 CEA, Annual Report of the Council, 2016 (commonly known as the “Economic Report of the President”).

4 Other factors, such as exchange rates, also negatively affected U.S. exports, as discussed throughout this report.

5 The “Energy and Related Products“ webpage of this report provides a summary of the sharp declines in the value of U.S. imports and exports of energy-related products in 2015. Trade of goods in other sectors was also affected by lower petroleum prices, as briefly described in the “Chemicals and Related Products,” “Electronic Products,” “Machinery,” “Minerals and Metals,” and “Transportation Equipment“ webpages. The analyses of U.S. trade with NAFTA partners, Brazil, Russia, and RCEP members also include some discussion of the impact of the crude petroleum price drop.

6 Spot prices tend to be more volatile than the longer-term contract pricing that many consuming industries use to hedge against short-term volatility. Unexpected supply disruptions, such as refinery shutdowns, can impact prices for consuming industries. See the “Energy and Related Products“ webpage for a discussion of examples of supply disruption in 2015.

7 Short- to long-term supply and demand expectations also affect the pricing of crude petroleum.

8 Inventories and storage capacity moderate the impact of supply or demand shocks on prices, since markets can draw down inventories if prices rise, or increase them if prices fall.

9 Crude petroleum is an inelastic good. Elasticity is an economic measure of the change in quantity supplied or demanded of a good to a change in price. If quantity demanded for a good responds more than proportionately to the change in price, the price elasticity of demand is greater than 1 and the relationship is said to be elastic. If demand responds less than proportionately to the change in price, the price elasticity of demand is less than 1 and is considered inelastic. See also “Deardorff’s Glossary of International Economics.”

10 The factors mentioned in this section are taken from Arezki and Blanchard, “The 2014 Oil Price Slump,” 2015; Sheppard, “The Five Main Drivers of Oil Prices,” April 5, 2016; Baffes et al., “The Great Plunge in Oil Prices,” 2015; Baumeister and Kilian, “Forty Years of Oil Price Fluctuations,” 2016; Tokic, “The 2014 Oil Bust: Causes and Consequences,” 2015.

11 Arezki and Blanchard, “The 2014 Oil Price Slump,” 2015; Baffes et al., “The Great Plunge in Oil Prices,” 2015, 20; IMF, World Economic Outlook, April 2016,15; see also Murphy, Plante, and Yucel, “Plunging Oil Prices,” 2015.

12 Killian specifically disagrees with Arezki and Blanchard regarding the role supply factors mentioned above, such as higher production in the United States, Libya, and Iraq, or decisions by OPEC to maintain production levels. See Baumeister and Kilian, “Understanding the Decline in the Price of Oil,” 2016; Kilian, “Causes of the 2014 Oil Price Decline,” 2015.

13 Baumeister and Kilian, “Understanding the Decline in the Price of Oil,” 2016; Kilian, “Causes of the 2014 Oil Price Decline,” 2015; Kilian, “The Impact of the Fracking Boom,” 2016.

14 For example, an appreciating dollar stimulates exports by countries other than the United States, increasing demand for crude and thus potentially offsetting the crude price drop that the dollar’s appreciation purportedly caused. Additionally, the appreciation argument should apply equally to the dollar-denominated price of other commodities, but does not appear to do so. Baumeister and Kilian, “Understanding the Decline in the Price of Oil,” 2016, 138.

15 By contrast, retail natural gas prices fluctuated, but returned to approximately where they began for both regions. See International Energy Agency, Energy Prices and Taxes Quarterly Statistics: First Quarter 2016, 1 (accessed July 6, 2016).

16 Hartley and Rosthal, “The Relationship of Natural Gas to Oil Prices,” 2008; Brown and Yücel, “What Drives Natural Gas Prices?” 2008.

17 Ramberg and Parsons, “The Weak Tie between Natural Gas and Oil Prices,” 2012.

18 Price regulations and temporary oversupply by major producers are examples of factors that have influenced natural gas prices in recent years.

19 To analyze how these price declines affected the U.S. macroeconomy, this section considers how crude petroleum and natural gas drive each of the major components of real GDP (measured in terms of expenditures)—consumption (C), investment (I), government purchases (G), and net exports (exports minus imports, or X - M). These are the building blocks of real gross domestic product: GDP = C + I + G + (X- M). This analysis does not explicitly consider G, government purchases, although the effect of falling energy prices on government purchases should be similar to the effect on private consumption, C, presented below.

20 CEA, Annual Report of the Council, 2016, 55, table 2-i; the estimate is constructed directly from data on crude petroleum imports, the decline in crude prices, rig counts, and investment in oil and mining equipment. The report does not consider the indirect effects of lower energy prices.

21 These are only the direct effects of the decline in the price of imported crude petroleum.

22 The CEA analysis concerns only crude petroleum, not natural gas. Because imports of natural gas account for only a small part of U.S. consumption, the analogous effect of imported gas savings are likely to be very small.

23 Average active rig count in September 2014 was 1930, and fell to 711 by December 2015. Baker Hughes, North America Rotary Rig Count pivot table (February 2011–present) (accessed June 10, 2016).

24 Kilian, “Demand and Not All Oil Price Shocks Are Alike,” 2009, 1054.

25 Baffes et al., “The Great Plunge in Oil Prices,” 2015, 23.

26 Arezki and Blanchard, “The 2014 Oil Price Slump: Seven Key Questions,” 2015.

27 All data in this box are drawn from USDOC, BEA, “Regional Economic Accounts: Download,” selection “Annual Gross Domestic Product (GDP) by State, NAICS All GDP Components” (accessed June 2, 2016).

28 The impact has largely been driven by changes in extraction technology.

29 Based on 1997 State GDP in North American Industry Classification System (NAICS) codes 211 (oil and gas extraction), the traditional producers, in declining order of importance, are Texas, Louisiana, California, Alaska, and Oklahoma.

30 However, the drop in crude petroleum prices is not the only negative factor affecting their economies. Growth rates in some countries showed slowing in 2013, well before the crude price drop, because of the global economic slowdown and country-specific economic issues.

31 For details, see World Bank, 2013; Berument, Ceylan, and Dogan, 2010; and Feldkirchner and Korhonen, 2012, as cited by Baffes et al., “The Great Plunge in Oil Prices,” 2015.

32 Bank of Canada, “Monetary Policy Report January 2015,” 2015.

33 A decline in crude prices also leads to currency depreciation in major exporters, which would lower the price of their non-crude sectoral exports. This could increase the quantity of those exports from crude exporters. This impact is reflected in analyses presented in the “NAFTA,” “Chemicals and Related Products,” and “Machinery“ webpages of this report. Baffes et al., “The Great Plunge in Oil Prices,” 2015, 28.

34 In Venezuela, for example, where the crude petroleum sector accounts for a large share of GDP, U.S. exports of equipment for crude petroleum and natural gas production, transport, and refining accounted for a larger share of the decline in U.S. manufactured goods exports, as discussed below. Trade Data Services, Inc., Import Genius database (accessed April 26–May 4, 2016). Venezuela is experiencing substantial political and economic turmoil, but the fall in crude petroleum prices is also a major contributor to the current political and economic challenges. Renwick and Lee, “Venezuela's Economic Fractures,” July 1, 2016. For a discussion of other factors affecting U.S. exports to Russia, including economic sanctions, see the “Russia“ webpage.

35 The asymmetry of gains between importers and exporters of crude continues to be a subject of research. Baffes et al., for example, hypothesizes that this asymmetry could be caused by uncertainty, market frictions, and varying monetary policy responses. Baffes et al., “The Great Plunge in Oil Prices,” 2015, 23.

36 See World Bank, 2013; Rasmussen and Roitman, 2011, as cited in Baffes et al., “The Great Plunge in Oil Prices,” 2015, 28.

37 See Constantinescu, Mattoo, and Ruta, Global Trade Watch: Trade Developments in 2015, 2016.

38 This section examines trade by North American Industry Classification System (NAICS) codes, which more closely match to manufacturing sectors related to crude petroleum and natural gas than do the digests used elsewhere in this report.

39 This section will focus on the effects of crude petroleum and natural gas prices on U.S. exports, but other factors also affected trade in 2015.

40 USITC DataWeb/USDOC, NAICS 321, 327, and 33 (accessed April 26, 2016).

41 The decline in prices started in 2014, but did not have an immediate impact on demand for equipment. Order backlogs contributed to higher revenues in 2014, but in 2015, as companies worked through their backlogs, the effects of declining capital expenditures by petroleum companies had a more significant impact on revenues. Brinkman et al., “Quarterly Perspective on Oil Field Services and Equipment,” November 2015, 4; Sulzer, “Full Year 2015 Results Presentation,” February 25, 2016, 6–7.

42 Baker Hughes, Worldwide Rig Counts—Current and Historical data, June 7, 2016.

43 This only includes products for which there is a 10-digit Schedule B classification specific to the oil and gas industry. As discussed below, this likely represents a small share of exports of products for oil and gas production.

44 USITC DataWeb/USDOC (accessed April 26, 2016).

45 Oil well and oil field pump manufacturers report significant negative impacts from declining oil and gas field expenditures. Sulzer, “Full Year 2015 Results Presentation,” February 25, 2016, 5, 20–24; ITT Corp, “2015 Earnings Call,” February 12, 2016, 11. U.S. exports of reciprocating oil well and oil field pumps (classified in the Harmonized Tariff Schedule of the United States, or HTS, as 8413.50.0010) declined by $215 million (26 percent), and exports of rotary positive-displacement oil well and oil field pumps (HTS 8413.60.0050) declined by $73 million (75 percent). These are the only types of pumps specifically identified in Schedule B as being for use in oil well and oil field applications, but it is likely that a decline in exports of other oil-related pumps contributed to the $738 million overall decline in U.S. pump exports (NAICS 333911). USITC DataWeb/USDOC (accessed February 2016).

46 USITC DataWeb/USDOC (accessed February 2016).

47 Includes imports by the South American-based operations of the five large oil service and equipment companies (Schlumberger, Baker Hughes, Halliburton, Weatherford International, and National Oilwell Varco) and the largest crude petroleum producer in each country (YPF in Argentina, Ecopetrol in Colombia, Empresa Estatal Petróleos del Ecuador, and Petróleos de Venezuela, S.A.). Trade Data Services, Import Genius database (accessed April 26–May 4, 2016). Although the overall economic climates in some of these countries were generally volatile in 2015 for various reasons, declining petroleum prices were a significant factor in weak demand for power generation equipment. Caterpillar Inc., “4Q 2015 Earnings Release,” January 28, 2016, 1–2; Trade Data Services, Import Genius database (accessed April 26–May 4, 2016).

48 Import Genius data do not include other ports in India. Trade Data Services, Inc., Import Genius database (accessed July 27, 2016).

49 USITC DataWeb/USDOC, https://dataweb.usitc.gov (accessed April 26, 2016).

50 See the “Chemicals and Related Products“ webpage for further discussion of the impact of crude petroleum and natural gas price declines on export values. As discussed in the individual sector write-ups, other non-price factors may also have affected exports of these products.

51 IHS, “Global Oversupply of Polyethylene,” May 16, 2016. As noted in figure ST.1, U.S. natural gas prices are lower than in many other major chemical-producing regions.

52 PPI measures the average change over time in selling prices received by producers for their output. The quantity of synthetic rubber exports declined 1.6 percent, and the unit value of exports declined 10 percent. The PPI for synthetic rubber declined 12 percent. USDOL, BLS, PPI databases, “Commodity Data” (accessed May 5, 2016); USITC DataWeb/USDOC (accessed May 5, 2016).

53 As noted earlier, the extent to which prices for plastic products correlate with resin prices varies by product. USDOL, BLS, PPI databases, “Commodity Data” (accessed May 5, 2016); Goldsberry, “If Oil Is So Cheap,” February 25, 2016.

54 USITC DataWeb/USDOC (accessed May 5, 2016).

55 Price changes for plastic products often trail price changes for resins. USDOL, BLS, PPI databases, “Commodity Data” (accessed May 5, 2016); Goldsberry, “If Oil Is So Cheap,” February 25, 2016.

56 USITC Dataweb/USDOC data indicate a 0.6 percent decrease ($12.1 billion) to $1.94 trillion in 2015 compared to 2014 (data accessed April 26, 2016).

57 The U.S. rig count fell 62 percent from December 2014 to December 2015. Baker Hughes, Worldwide Rig Counts—Current and Historical Data, June 7, 2016.

58 The definition of consumer goods is based on the United Nations Conference on Trade and Development (UNCTAD) list of HS 6-digit subheadings, excluding goods in chapter 27 and any products that are not considered manufactured goods in the NAICS. Since this list is at the HS 6-digit level, it likely includes some products that are not typically considered consumer goods but are part of a broad subheading. For the list of goods, see the World Bank Website, http://wits.worldbank.org/referencedata.html (accessed June 1, 2016).

59 USITC DataWeb/USDOC, (accessed June 1, 2016).

60 U.S. personal consumption expenditures rose in each quarter in 2015. USDOC, BEA, “Table 2.3.3. Real Personal Consumption Expenditures by Major Type of Product, Quantity Indexes,” May 27, 2016.

61 USITC DataWeb/USDOC (accessed June 1, 2016).

62 CEA, Economic Report to the President, 2016.