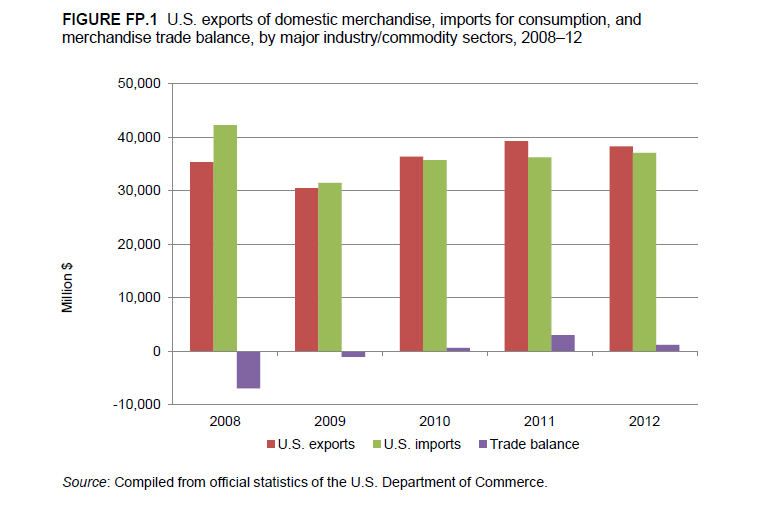

Change in 2012 from 2011:

- U.S. trade surplus: Decreased by $1.8 billion (60 percent) to $1.2 billion

- U.S. exports: Decreased by $965 million (2.5 percent) to $38.3 billion

- U.S. imports: Increased by $845 million (2.3 percent) to $37.1 billion

For the third consecutive year, the United States experienced a trade surplus in forest products in 2012, although the surplus declined from 2011. Over the past five years, the trade balance in forest products has trended from a deficit of $6.9 billion in 2008 to a surplus of over $3.0 billion in 2011, with the surplus then declining to $1.2 billion in 2012 (figure FP.1). Generally, increases in imports during 2012 mirrored the slow but steady recovery in U.S. housing construction, while overall decreases in exports reflected slower growth in China and Europe.

While trade with NAFTA partners Mexico and Canada represented about 40 percent of U.S. forest products exports and 48 percent of U.S. forest products imports, trade with China shifted the most in 2012. China is the second-largest U.S. export market for forest products behind Canada; it accounts for 16 percent of the total. China is also the United States’ second-largest source of forest products imports, accounting for 22 percent of the total, also behind Canada. U.S. forest products exports to China declined by 8 percent ($514 million) in 2012, while U.S. imports from China increased by 10 percent ($747 million). Less robust growth in the Chinese economy in 2012 was the chief reason for the decline in U.S. exports. Other market factors also played a role, including increases in the Chinese paper recovery rate (affecting its imports of recovered paper) and the availability of more competitive softwood lumber supplies from other countries. Conversely, notable increases in U.S. imports of wood panels from China, as the U.S. economy gradually recovered, contributed to a widening of the U.S. trade deficit with that country.

The trade surplus in forest products masks some variability in trade by commodity and trading partner. A strong export market for U.S. hardwood lumber in Asia (notably in China, Vietnam, and Japan) was not enough to offset higher U.S. imports of softwood lumber from Canada, spurred by an improvement in U.S. housing construction.

U.S. Exports

The total value of U.S. forest products exports in 2012 declined by $965 million, or 2 percent. The largest absolute trade shift among forest products exports occurred in exports of wood pulp and recovered paper, which fell by $810 million (8 percent), primarily due to decreased demand in China. Chinese paper production expanded at a slower rate last year and relied on more domestic sources of raw materials and recovered paper. The Chinese economy in general grew at a somewhat slower rate during 2012 (8 percent) than during 2011 (9 percent) and previous years. Accordingly, U.S. exports of wood pulp and recovered paper to China declined by over $200 million.The second-largest absolute shift occurred with respect to U.S. exports of paperboard, which decreased by $393 million, or 6 percent. Paperboard is mainly used for packaging, and the decrease in exports can again be largely attributed to the weaker economies in China and the European Union (EU).

While the value of U.S. exports of coniferous (softwood) and non-coniferous (hardwood) logs declined moderately in 2012, along with exports of softwood lumber, the value of U.S. hardwood lumber exports increased by nearly 10 percent, reaching a five-year high at $1.6 billion. U.S. hardwood lumber species are increasingly favored for use in the Chinese architectural woodwork, flooring, and furniture industries, and have become particularly competitive in China against other temperate and tropical lumber varieties. The Lacey Act amendments and a new EU timber regulation, both aimed at reducing trade in illegally harvested and traded wood products, are also encouraging Asian and EU hardwood buyers to use American hardwoods rather than tropical wood species deemed to pose a higher sourcing risk.

U.S. forest products exports to the EU were generally lower in 2012 because of Europe’s weaker economy, a stronger U.S. dollar compared to the euro, and, for paper and paperboard, excess European capacity. One exception involved a significant increase in U.S. exports of wood pellets — used for fueling power plants and other energy facilities — to the EU. U.S. wood pellet export capacity has been increasing rapidly, with exports valued at $207.1 million in 2012, and the EU accounted for 93 percent of those exports. An important reason for the expanded exports is the EU renewable energy directive aiming to achieve a 20 percent share of energy from renewable sources by 2020. This directive has stimulated demand for wood pellets, many of which are being sourced from outside of Europe. Reportedly, many European energy producers are entering into long-term supply agreements with U.S. wood pellet producers.

U.S. Imports

Wood pulp and recovered paper represented the largest trade shift in forest products imports, with a decrease of $674 million or 17 percent. This mirrored, to some extent, a decline in exports (8 percent) in this commodity group, suggesting that some of the shipments that previously may have been exported were redirected into the U.S. market, thus reducing demand for imports.

U.S. housing starts rose by 28 percent in 2012, to 781,000 units, prompting an increase in U.S. wood products production, import demand, and prices. The total value of U.S. forest products imports increased by $845 million (2 percent) in 2012. Canada continued to be the largest source of imports, accounting for 44 percent of the total in 2012, but its share has declined over the past decade. Canada accounted for nearly one-half of U.S. forest products imports as recently as 2008. In contrast, forest products imports from China, the second-largest supplier to the United States, have been increasing in both absolute and relative terms, accounting for 22 percent of the total in 2012.

U.S. paper demand weakened in 2012, particularly for printing and writing grades that use imported hardwood pulp. U.S. trade in pulp and paper products has been gradually affected by long-term trends in consumption. Over the past decade, electronic communications have significantly lowered U.S. demand for newsprint and printing/writing papers, triggering a gradual decline in imports of these paper grades.

In contrast to imports of wood pulp, recovered paper, and many paper grades, which declined, imports of most lumber and solid wood products increased in 2012 on increased U.S. demand from the housing construction industry. The value of U.S. lumber imports in 2012 rose 18 percent, while volume increased 5 percent. Wood veneer and panels also accounted for a large increase in the value of forest products imports, with imports from China accounting for most of the $668 million, or 21 percent, growth in this commodity group. Plywood imports from China in particular rose in volume and value, with unit values rising from $501 per cubic meter in 2011 to $548 per cubic meter in 2012. Plywood and flooring shipments from Indonesia, Malaysia, Vietnam, and parts of South America (i.e., Ecuador and Paraguay) also increased significantly, while imports from Brazil declined.