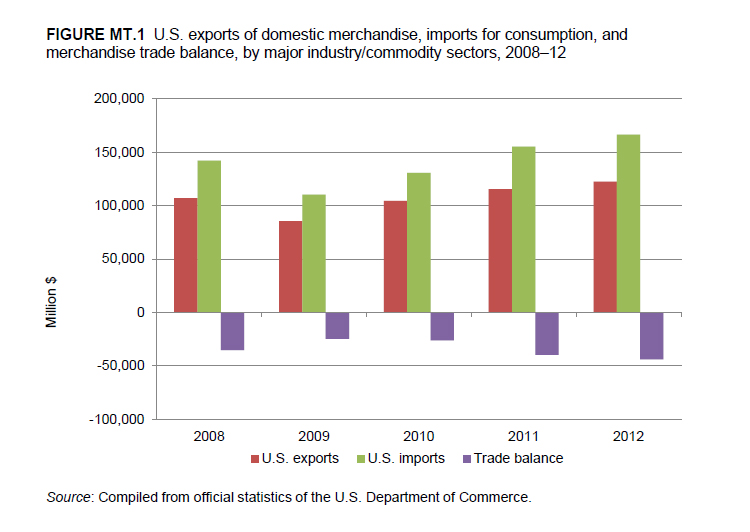

Change in 2012 from 2011:

- U.S. trade deficit: Increased by $4.1 billion (10 percent) to $43.8 billion

- U.S. exports: Increased by $7.2 billion (6 percent) to $122.4 billion

- U.S. imports: Increased by $11.3 billion (7 percent) to $166.2 billion

In 2012, the U.S. merchandise trade deficit in machinery increased to $43.8 billion, as domestic imports exceeded exports by $4.1 billion (Figure MT.1). Higher U.S. exports of machinery were principally due to a weakening U.S. dollar in certain major markets which made U.S. farm and garden machinery more price competitive, and to U.S. competitiveness in the production of electric generating sets. The import growth within this sector reflected growth in complementary industries, including the transportation equipment sector, given that the machinery sector produces critical inputs used in various manufacturing industries.

U.S. Exports

In 2012, U.S. exports of machinery rose by $7.2 billion (6 percent) to $122.4 billion, with major shifts occurring in farm and garden machinery; electric motors, generators, and related equipment; and pumps for liquids. By destination, Mexico, Canada, and a number of smaller export markets (particularly Australia, Venezuela, Saudi Arabia, and Russia) accounted for the largest increases in the value of U.S. exports of machinery. The largest declines in U.S. exports were to China, Japan, Germany, and Hong Kong.

The largest absolute shift in machinery exports was the $1.9 billion increase in U.S. exports of farm and garden machinery (up 17 percent to $13.1 billion). This growth was driven largely by absolute increases in exports to Canada, Australia, and Brazil. The weaker U.S. dollar relative to the currencies of these three economies in particular made U.S. exports more competitive. Rising agricultural commodity prices and strong farm income and government support programs in most foreign markets, which strengthened demand for U.S. exports of farm and garden machinery, were also a factor.

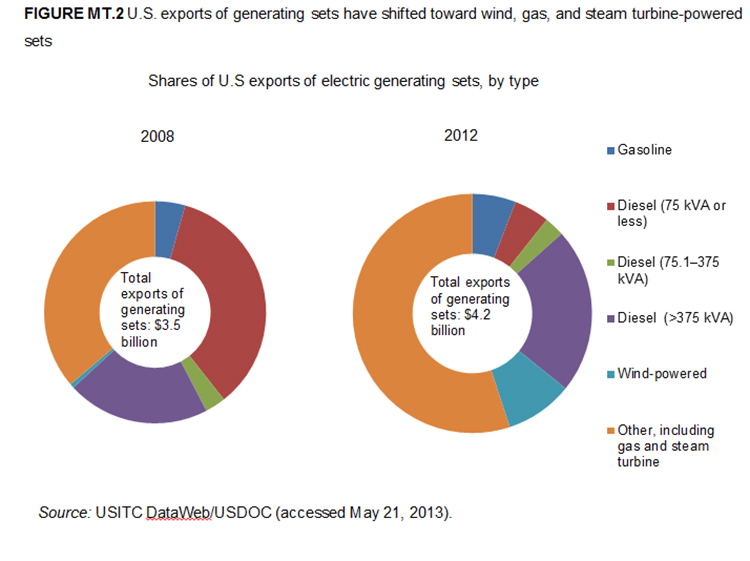

The second-largest absolute shift in machinery exports involved electric motors, generators, and related equipment, which rose by $1.4 billion (18 percent) to $9.3 billion in 2012. Canada and Mexico remained the largest and second-largest markets, respectively, for U.S. exports of these goods. The increase was driven largely by higher exports of electrical generating sets (typically a steam- or gas-powered turbine combined with an electric generator) and wind turbines (a wind turbine with an electric generator).

Electric generating sets accounted for $660 million in U.S. exports of electric motors, generators, and related equipment in 2012 — almost half of the increase in this category — with Venezuela, Australia, and Russia being the leading U.S. markets for these products. These electric generating sets are typically used in the oil, gas, or mining industries, or in mobile or backup electric power generation applications. The United States has a globally competitive electric generator set industry. Wind turbines accounted for $261 million of the increase in exports of electric motors, generators, and related equipment, and was the second leading export product. Exports of wind turbines went principally to Mexico to equip new wind farms.

U.S. exports of pumps for liquids increased by $896 million (15 percent) to $7.1 billion. The leading type of pump exported was centrifugal pumps, which accounted for almost one-third of exports. Such pumps are used in industrial, chemical/petroleum, water handling, greenhouse, hygienic, and marine applications. The major markets for these products were for power and energy and industrial end markets in North and South America and for food and beverage and industrial end markets in the Asia/Pacific region. Some of these sales were for the aftermarket in the Americas, the Middle East, and the Asia/Pacific region, but sales of aftermarket pumps to Europe were weak because of the soft European economy. Exports of pumps to Canada, the largest market for U.S. exports of these products, rose by $237 million to $1.9 billion. Mexico was the second-largest market, and U.S. exports to Mexico rose by $106 million to $681 million.

The gains in U.S. machinery exports in 2012 were offset by a decline in U.S. exports of semiconductor manufacturing equipment, which fell by $1.1 billion (8 percent) to $13.6 billion. Semiconductor manufacturing equipment markets in all regions — except Taiwan and Korea — were significantly weaker in 2012, as reflected in reduced U.S. exports to China, Japan, and other large markets during that year. The decline in these markets was due to weaker unit demand for semiconductors that led producers in these countries to curtail their capital expenditure plans, as well as a lack of new large projects in progress in 2012. Nevertheless, U.S. exports to Taiwan and Korea increased due to continued investments in semiconductor fabrication plant expansions and equipment upgrades used to produce the next generation of semiconductors.

U.S. Imports

U.S. imports of machinery increased by $11.3 billion (7 percent) to $166.2 billion in 2012. Imports of machinery from virtually all suppliers increased, with China and Mexico representing the largest sources of U.S. imports within this sector.

The largest increase in U.S. machinery imports occurred in metal-cutting machine tools, which rose by $1.3 billion (29 percent) to $5.8 billion in 2012. The increase in imports of metal-cutting machine tools was likely due to demand from motor vehicle, aerospace, medical, and general machinery manufacturers, which were upgrading plants as they experienced strong demand for their products. Imports from Japan led the shift in this sector, increasing by $426 million to $2.3 billion, followed by imports from Germany, which rose by $252 million to $969 million. Imports from Taiwan rose by $173 million to $525 million. Notably, imports from Korea rose by $175 million (58 percent) to $475 million and likely benefited from the elimination of U.S. tariffs on these products (which ranged from 3 to 4 percent ad valorem) under the U.S.-Korea free trade agreement in 2012.

The second-largest increase in imports was of taps, cocks, valves, and similar devices, which rose by $1.3 billion (11 percent) to $13 billion. The leading import products responsible for this shift were other valves (including solenoid valves, of which motor vehicle fuel injectors are a subset), parts for valves, and check (nonreturn) valves. Sophisticated fuel injectors for automobiles and heavy-duty engines are increasingly being imported. Leading sources were China, Mexico, and Japan, all of which registered import increases in this commodity group in 2012.

U.S. imports of air-conditioning equipment and parts increased in absolute terms by $1.2 billion (10 percent) as imports of these articles from China rose by $555 million and from Mexico by $364 million. Warm temperatures in the spring and summer of 2012 increased demand for both air-conditioning equipment and imported parts used in the production of such equipment. Shipments into the United States of central air conditioners and air-source heat pumps rose by almost 5 percent in 2012, rising from 3.7 million units to 3.9 million units. Increased imports from China principally consisted of window air-conditioning equipment, ceiling and other fans, compressors and parts, motor vehicle air-conditioning machines, other parts of air-conditioning machines, and other air-conditioning machines. Increased imports from Mexico primarily comprised parts of air-conditioning machines, particularly for motor vehicles, for motor vehicle turbochargers and superchargers, and for other air-conditioning machines.

Other significant increases in U.S. imports of machinery occurred in electric motors, generators, and related equipment; farm and garden machinery; and household appliances, including commercial appliances. The increase in U.S. imports of machinery was offset by declining imports of semiconductor manufacturing equipment, which fell by $1.1 billion to $13.1 billion. Imports of such equipment from Japan fell by $613 million and from the Netherlands by $526 billion. The decline likely was related to the completion of major semiconductor equipment upgrades in 2012 at semiconductor plants of Intel and Samsung Austin Semiconductor, as well as the global downturn in semiconductor production in 2012.