Karl Tsuji

(202) 205-3434

karl.tsuji@usitc.gov

Change in 2013 from 2012:

- U.S. trade deficit: Increased by $2.5 billion (4.7 percent) to $56.7 billion

- U.S. exports: Decreased by $6.8 billion (4.8 percent) to $133.7 billion

- U.S. imports: Decreased by $4.2 billion (2.2 percent) to $190.5 billion

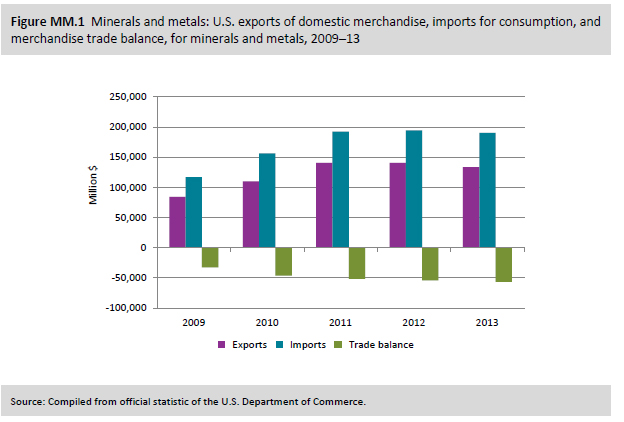

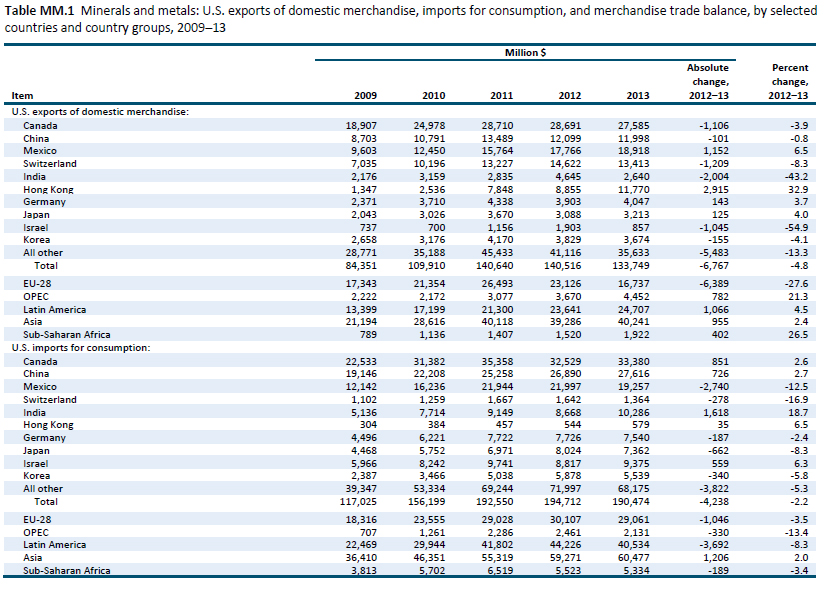

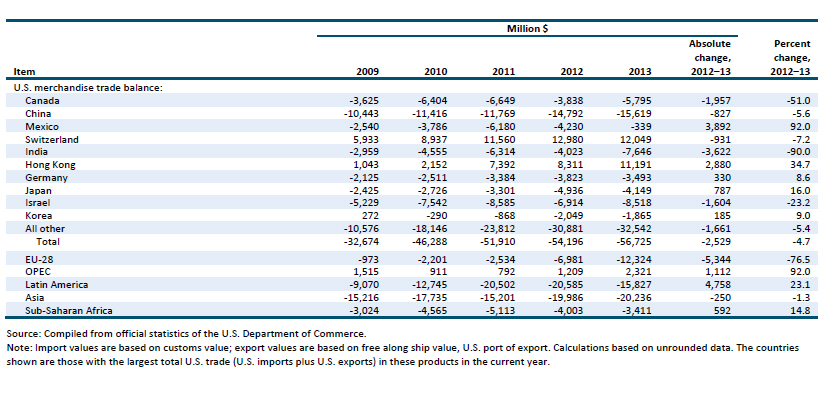

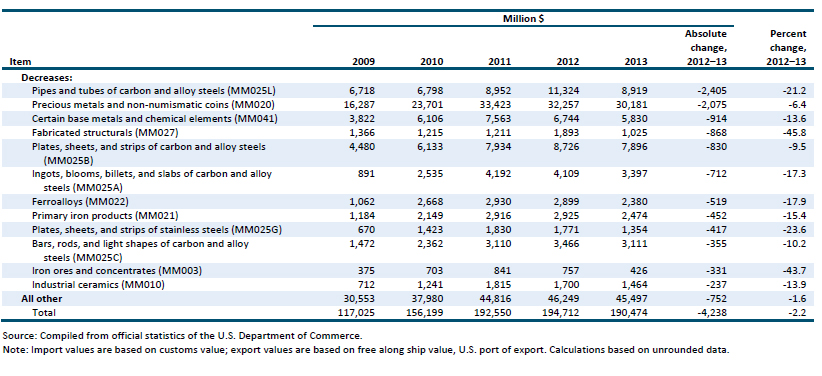

In 2013, both U.S. exports and U.S. imports of minerals and metals decreased, and since the decline in exports exceeded the decline in imports, the U.S. trade deficit in this category continued to widen. The United States has maintained a trade deficit in minerals and metals in each successive year since 2009 (figure MM.1). During this five-year period, the U.S. trade deficit widened the most with China (by $5.2 billion), followed by India ($4.7 billion), Israel ($3.3 billion), and Canada ($2.2 billion) (table MM.1). Leading shifts among U.S. imports and exports of minerals and metals over 2009––13 (table MM.2) reflected the economic performance of the major downstream consuming industries. Of particular importance were recovering construction activity, varying growth rates among individual durable-goods manufacturing industries, and continued rising energy production. Such shifts also resulted from shortfalls in domestic mine resources for many critical raw materials and generally lower commodity prices.

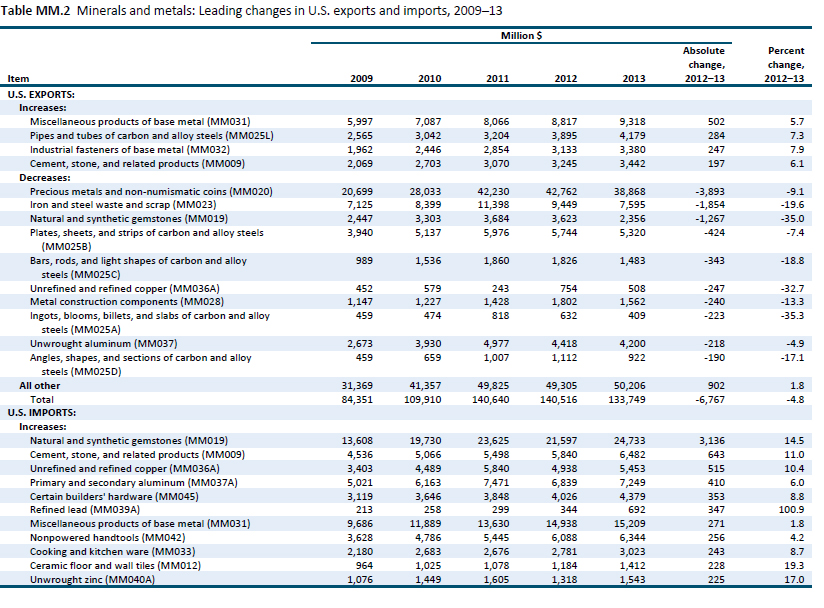

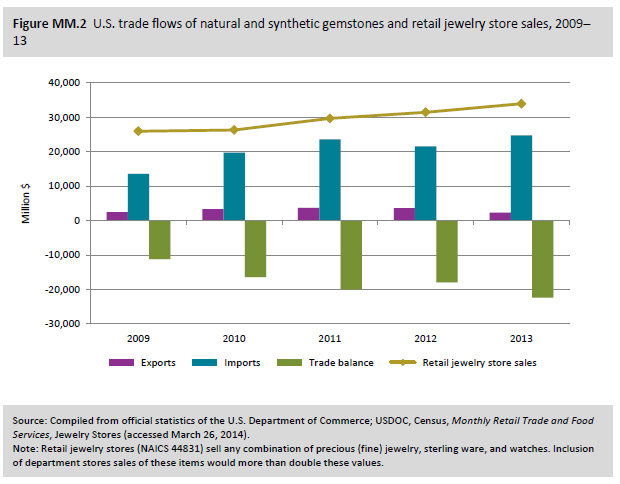

Among the leading changes for U.S. trade in minerals and metals in 2012–13 were significant shifts in both U.S. exports and U.S. imports of natural and artificial gemstones and precious metals and non-numismatic coins (table MM.2). U.S. trade in natural and artificial gemstones significantly contributed to widening the U.S. trade deficit for minerals and metals between 2012 and 2013; the deficit grew by $4.4 billion (24 percent) to $22.4 billion (figure MM.2). On the one hand, U.S. exports of natural and artificial gemstones decreased by $1.3 billion (35 percent) to $2.4 billion in 2013, with the largest decreases recorded to Israel, followed by India. On the other hand, U.S. imports of these goods increased by $3.1 billion (15 percent) to $24.7 billion, with the largest increases recorded from India, followed by Israel and Belgium. India is one of the world’s largest centers for the processing (cutting and polishing) of diamond and colored gemstones and for the making of precious jewelry, and Israel and Belgium are both major diamond processing and trading centers.

Nonindustrial (gem-quality) diamonds—worked, but not mounted or set—accounted for most of the U.S. trade shifts for gemstones. The decrease of $1.2 billion in the value of exports reflected lower quantities shipped, while the increase of $3.0 billion in the value of imports reflected higher imports of higher-priced, larger diamonds (weighing more than 0.5 carat each) rather than lower-priced, smaller ones (not more than 0.5 carat each).

Industry observers’ anticipation in first quarter 2013 that U.S. retail sales of precious jewelry and watches would continue growing from 2012 levels was fulfilled by reports of robust year-end holiday sales. Lacking domestic mined-diamond resources, the United States was almost totally dependent upon imports to meet increased downstream consumption needs of precious jewelry manufacturers.

U.S. Exports

Although U.S. exports of minerals and metals decreased by $6.8 billion (4.8 percent) to $133.7 billion in 2013, certain products recorded increased exports (table MM.2). The leading U.S. export was miscellaneous products of base metal, which increased by $502 million (6 percent) to $9.3 billion. The United States’ NAFTA partners (Canada and Mexico) were the leading U.S. destination markets for these products in 2013, with Mexico recording the largest increase in exports, up $205 million (8 percent) to $2.7 billion. U.S. exports to NAFTA partners reflect the extensive integration of the North American manufacturing industry through production-sharing arrangements and cross-border ties. Specific products in this category that recorded the largest export increases included miscellaneous iron or steel articles (up by $246 million); miscellaneous aluminum articles (up by $147 million); and base-metal hinges, castors, mountings, and fittings (up by $135 million). U.S. exports of miscellaneous base-metal products increased concurrently with the growth in shipment values reported by durable-goods manufacturers, either of finished base-metal products or of downstream products that contain intermediate base-metal products.

Precious metals and non-numismatic coins recorded the leading U.S. export decrease by value, down $3.9 billion (9 percent) to $38.9 billion. The largest decreases in exports were to the United Kingdom and Switzerland—major global centers for refining, fabricating, and trading of all precious metals—and India, a major precious-jewelry fabricating and consuming market. Gold accounted for most of this export decline, as exports of unwrought gold (as unrefined doré and refined bullion) decreased by $1.8 billion, while gold waste and scrap exports decreased by $1.4 billion.

In addition to the smaller quantity of gold exported in 2013, the price for gold also decreased in 2013, further reducing the value of gold exports. Some financial-market observers attributed the decrease in gold prices to the fact that investors were less concerned about potential inflation.

As the world’s largest and most highly industrialized economy, with a well-established, nationwide scrap recovery infrastructure, the United States is the world’s leading generator of ferrous (iron and steel) scrap, with production levels far exceeding domestic consumption needs. However, the value of U.S. exports of iron and steel waste and scrap decreased by $1.9 billion (20 percent) to $7.6 billion. This decline reflected both lower quantities exported and weaker prices. The lower export quantities were attributed by industry observers to competition with scrap production in foreign markets; the weaker prices, to overcapacity among domestic scrap generation and processing operations. Turkey, followed by Taiwan, India, Korea, China, and Malaysia, accounted for the largest decreases in U.S. exports (in excess of $100 million each). All six trading partners have large steel industries, and each is highly dependent upon foreign sources of ferrous scrap for their steelmaking industries. However, all six trading partners imported less ferrous scrap from the world in 2013 than in the previous year, although their reasons varied: crude-steel output decreased in Turkey and Korea, but crude-steel producers in Taiwan, India, China, and Malaysia shifted to other types of ferrous raw materials for their increased output.

U.S. Imports

Overall, U.S. imports of minerals and metals declined by $4.2 billion (2.2 percent) to $190.5 billion in 2013. Contributing significantly to this decline were imports of pipes and tubes of carbon and alloy steels (table MM.2), which decreased by $2.4 billion (21 percent) to $8.9 billion. Japan, followed by Germany, Canada, the UK, India, Russia, and China, accounted for the largest decreases in U.S. imports (in excess of $100 million each) in 2013. This decrease reflected both weaker prices and lower import quantities during a period when U.S. domestic consumption of steel pipe and tube also decreased. Lower activity levels in the leading end-use markets were cited by some industry observers as dampening domestic demand for line pipes.

The value of U.S. imports of precious metals and non-numismatic coins fell by $2.1 billion (6 percent) to $30.2 billion, with the largest decreases recorded from Mexico, followed by Colombia, Bolivia, and South Africa—all major precious-metal mining countries. Gold accounted for most of this decline, with the value of imports of unwrought gold down by $1.8 billion and that of imports of gold waste and scrap down by $354 million. As the quantity of gold imports actually increased in 2013, the decreased value of U.S. imports was caused solely by significantly lower gold prices. The lower prices, combined with improved consumer sentiment, spurred increased U.S. consumer demand in 2013 for precious jewelry and investment items (in the forms of bullion bars and non-numismatic coins), the largest end-use sectors for gold consumption.

U.S. imports of certain base metals and chemical elements (minor metals) decreased by $914 million (14 percent) to $5.8 billion. Nickel accounted for the largest import decrease (down by $505 million), with the largest decline from major mined-nickel producer Russia, followed by Australia. Import declines in 2013 reflected both lower quantities (owing to reduced domestic consumption) and weaker global prices, the result of reduced Chinese demand for ferronickel, European manufacturing cutbacks, and record accumulations of nickel in commodity exchange warehouses. Titanium accounted for the second-largest decrease (down by $182 million), with the largest decline from major unwrought (sponge) titanium producer Japan, followed by Kazakhstan and China. The value of U.S. titanium sponge imports declined, despite higher global sponge prices, because of lower import quantities caused by declining domestic demand for sponge as firms increasingly sought titanium scrap as a substitute.