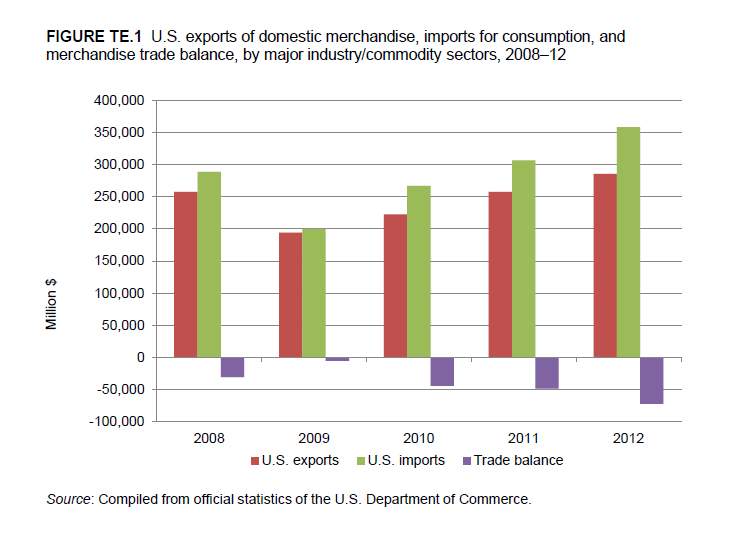

Change in 2012 from 2011:

- U.S. trade deficit: Increased by $119 million (0.1 percent) to $94.3 billion

- U.S. exports: Decreased by $222 million (1 percent) to $19.2 billion

- U.S. imports: Decreased by $103 million (0.1 percent) to $113.5 billion

In 2012, the U.S. trade deficit in textiles and apparel rose slightly to $94.3 billion, the result of a relatively small drop in U.S. exports that outweighed the small decline in U.S. imports (figure TX.1). Imports supplied most of U.S. consumer demand for textiles and apparel. While the average unit value of U.S. imports decreased slightly between 2011 and 2012, consumer spending on clothing increased by 5 percent, as a result of higher retail prices. In 2012, imports in three categories — shirts and blouses; trousers; and robes, nightwear, and underwear — together accounted for the largest share (43 percent) of U.S. textile and apparel imports, decreasing by 1 percent to $49.0 billion. Though U.S. exports of fabric continued to lead sector exports, the slight increase of 1 percent to $6.3 billion in 2012 was outweighed by decreases in U.S. exports of other major textile products, primarily fibers and yarns.

The United States continued to register a trade deficit with most of its major trading partners in this sector. Notably, the trade deficit with Honduras increased by $354 million (40 percent) to $1.2 billion in 2012. The only major exception was Canada, which is the second-largest export market for U.S.-made textile and apparel items. The United States registered a trade surplus of nearly $1.5 billion with Canada in this sector in 2012, having maintained a surplus every year during 2008-12. China supplied 40 percent of U.S. imports of textiles and apparel in 2012, remaining the largest supplier of these products.

U.S. Exports

U.S. exports of textiles and apparel decreased by $222 million (1 percent) to $19.2 billion in 2012. U.S. exports in this sector are largely composed of textile articles, which represent 82 percent of all U.S. exports of textiles and apparel. These exports are often used as intermediate inputs for finished products manufactured abroad, which are then imported back into the United States. The top markets for U.S. textile exports are partner countries in the North American Free Trade Agreement (NAFTA) or the Dominican Republic-Central America-United States Free Trade Agreement (CAFTA-DR); these countries collectively accounted for 61 percent of all such exports in 2012. In addition to preferential duty treatment, these partners benefit from shorter lead times because of their proximity to the U.S. market. Since much of the fibers, yarns, and fabric exported to NAFTA and CAFTA-DR partner countries re-enter the United States as finished garments, demand for U.S. exports of textiles is closely correlated to U.S. imports of apparel from these countries. U.S. exports of textiles to these trading partners declined by 4 percent between 2011 and 2012, which was partly reflected in a 1.2 percent decrease in U.S. imports of apparel from these countries during the same period (see discussion of U.S. imports below).

U.S. exports to its three leading export markets — Mexico, Canada, and Honduras — showed mixed results between 2011 and 2012. U.S. exports to Mexico rose by $87 million (2 percent) to $4.2 billion, and exports to Canada rose by $198 million (5 percent) to $3.9 billion. Meanwhile, U.S. exports to Honduras dropped by $384 million (21 percent) to $1.5 billion.

Exports of fibers and yarns experienced the greatest decline, of $552 million (10 percent) to $5.1 billion, while U.S. exports of fabric were largely unchanged. As these inputs are primarily used in the production of finished apparel, the decrease in U.S. exports reflects fewer shipments of inputs to apparel manufacturing facilities abroad.

U.S. Imports

For the first time since 2009, U.S. imports of textiles and apparel declined, falling by a modest 0.1 percent or $103 million to $113.5 billion in 2012. Imports from China, by far the largest supplier of textiles and apparel to the United States, were mostly flat, rising just 0.3 percent to $44.9 billion. In contrast to the substantial increases in U.S. imports of textiles and apparel from China each year between 2009 and 2011, the stable level of imports in 2012 largely reflects efforts by producers to diversify their supply chains by moving some manufacturing capacity from China to other Asian producers, notably Vietnam.

Compared with 2011, the value of U.S. apparel retail sales increased by nearly 6 percent in 2012. This increase reflects growth of $13.4 billion in consumer expenditures on garments. As U.S. imports of apparel by quantity, or square meter equivalents (SMEs), declined by 1 percent in 2012, higher sales volumes do not explain this growth. Instead, increased expenditures are likely attributable to retail inflation due to increased commodity input prices, rising wages in manufacturing countries (primarily China), and increasing freight costs.

U.S. imports from Asia, the largest regional supplier — accounting for three-quarters of all sector imports — decreased by $170 million (0.2 percent) to $84.7 billion in 2012. Imports from Pakistan accounted for much of the decline, falling by 10 percent to $3.1 billion. In 2012, textile and apparel production in Pakistan experienced major setbacks as a result of natural gas and electricity shortages. Approximately 40 percent of textile factories either shut down or ran at reduced capacity, and thousands of workers were laid off, cutting production and exports from the country. By contrast, U.S. imports from Vietnam increased by $418 million (6 percent), the only gain among the 10 largest suppliers. The United States is Vietnam’s largest export market for textiles and apparel.

U.S. imports from Latin America, comprising CAFTA-DR countries and Mexico, accounted for 14 percent of total sector imports in 2012 and fell by $219 million (1 percent). The decrease was primarily driven by imports from Mexico, which declined by $99 million (2 percent). Mexican safeguards against imports of textiles and apparel from China expired in December 2011, which intensified competitive pressures on the Mexican industry in 2012 Regional FTAs, including CAFTA-DR, also hampered the competitiveness of the Mexican industry.

Unlike U.S. exports, U.S. imports of textiles and apparel are largely composed of apparel, which represented three-quarters of all U.S. sector imports in 2012. By quantity, U.S. apparel imports were stable between 2011 and 2012, as a decrease in imports of cotton apparel was offset by a corresponding increase in imports of manmade-fiber apparel. Driven by volatile cotton prices, demand by apparel manufacturers shifted away from cotton in favor of relatively cheaper manmade fibers.

By value, apparel registered the largest overall change for U.S. imports — a decline of $706 million to $85.0 billion. This decline was driven by decreases in imports of shirts and blouses; women’s and girls’ suits, skirts, and coats; other wearing apparel; and men’s and boys’ coats and jackets. Within these subcategories, U.S. imports of shirts and blouses experienced the largest decline, falling nearly $700 million to $26.0 billion (3 percent).

Footwear

Change in 2012 from 2011:

- U.S. trade deficit: Increased by $1.2 billion (6 percent) to $22.9 billion

- U.S. exports: Decreased by $7 million (1 percent) to $824 million

- U.S. imports: Increased by $1.2 billion (5 percent) to $23.7 billion

In 2012, the U.S. trade deficit in footwear grew by $1.2 billion (6 percent), owing to a sizable increase in U.S. imports of $1.2 billion and a marginal decrease of $7 million in U.S. exports (table TX.3). Imports supplied over 95 percent of domestic demand in 2012. China was by far the largest supplier of footwear to the United States, accounting for 72 percent of all U.S. footwear imports. However, other Asian producers, particularly Vietnam and Indonesia, continued to steadily increase their share of the U.S. market at China’s expense. Though U.S. exports declined slightly in 2012 from a peak of $832 million in 2011, the 2012 level was the second-highest during the past five years.

While U.S. exports to most major export destinations decreased moderately in 2012, exports to Canada, the largest export market, increased by $22 million.Consumer spending on footwear increased by 5 percent between 2011 and 2012. According to industry sources, expenditures on women’s footwear led this growth, particularly spending on shoes, sandals, and lightweight running shoes. However, for many products, higher consumer expenditures were mostly the result of higher retail prices, as rising materials, transportation, and labor costs were passed on to consumers. For example, while revenues from athletic shoes increased by 4 percent in 2012 compared with 2011, unit sales were flat.

U.S. Exports

Canada and the Republic of Korea (Korea) were the top two export markets for U.S. producers; these countries accounted for 14 percent and 12 percent, respectively, of U.S. exports of footwear by value in 2012. U.S. exports of footwear to its largest market, Canada, increased by the greatest percentage and amount, up $22 million (24 percent) to $116 million. U.S. exports to Korea, meanwhile, increased by $7 million (7 percent) to $101 million. Other important markets for U.S. footwear exports in 2012 were Japan, Mexico, and Hong Kong. U.S. exports to most major export destinations decreased moderately.

Exports are a significant source of revenue for domestic footwear manufacturers, accounting for an estimated 38 percent of industry revenues in 2012. U.S. production of footwear is largely concentrated in niche markets — rubber/fabric footwear, men’s work shoes, and plastic/protective footwear. These products are technologically advanced, meet particular health, defense, and safety standards, and have garnered a reputation for quality in major export markets. Footwear parts, including removable insoles, heel cushions, and gaiters, made up about one-quarter of U.S. exports in 2012. Such exports are generally used to assemble final goods overseas.

U.S. Imports

U.S. imports of footwear increased by $1.2 billion (5 percent) to $23.7 billion in 2012. This growth was driven by imports from Asia, which increased by nearly $1 billion ($942 million) between 2011 and 2012, particularly from China, Vietnam, and to a lesser extent, Indonesia. The largest absolute increases were in imports from China and Vietnam, the two leading U.S. suppliers. Nearly three-quarters (72 percent) of U.S. imports of footwear in 2012 were supplied by China. However, many footwear companies are employing a “China plus one” sourcing strategy in order to diversify their supply chains, expanding into nearby countries such as Vietnam and Indonesia. U.S. imports from Vietnam and Indonesia grew by 134 percent and 130 percent, respectively, during 2008-12 and by 18 percent and 23 percent in 2012 over 2011, respectively.

Because the footwear industry is highly labor intensive, many U.S. producers have shifted production to low-cost countries, maintaining branding and design capabilities in the United States. For example, Nike produced 98 percent of its footwear overseas in 2012. Between 2007 and 2012, the number of domestic footwear manufacturing facilities declined from 1,050 to 721 and the workforce declined from 15,761 to 11,581.

While Asian producers supply low-cost shoes, Italy specializes in high-end shoes and fashion footwear that use expensive inputs (especially leather) and command a price premium. Thus, Italy continues to be an important supplier to the high-end U.S. market and remained the third-largest supplier of footwear to the United States in 2012, growing by 8 percent over 2011.