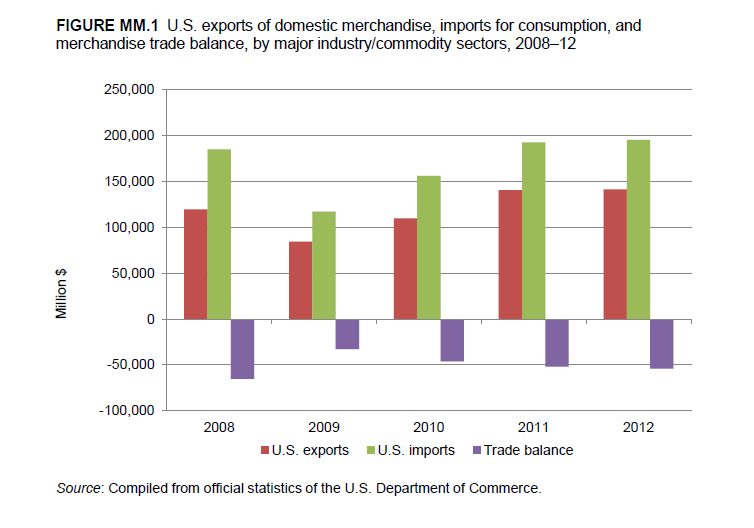

Change in 2012 from 2011:

- U.S. trade deficit: Increased by $2.1 billion (4 percent) to $54.2 billion

- U.S. exports: Decreased by $0.1 billion (-0.1 percent) to $140.5 billion

- U.S. imports: Increased by $2.2 billion (1.1 percent) to $194.7 billion

In 2012, U.S. imports of minerals and metals increased slightly over 2011 levels, while exports were largely flat, resulting in a $2.1 billion widening of the deficit in this commodity group (figure MM.1). This was in contrast to the previous year, when exports increased by 27 percent and imports by 23 percent over 2010 levels. The very slight decline in exports principally reflected higher prices in key commodities, such as gold, as opposed to global demand shifts. Heightened U.S. imports partly resulted from increased gold prices as well, but also reflected a need to support U.S. domestic oil and gas production and motor vehicle manufacturing; imports from this sector are critical inputs to these industries.

U.S. Exports

The slight decline in U.S. exports of minerals and metals was driven by lower exports of gold bullion (gold of a certain recognized purity level) and a sharp drop in exports of gold and silver scrap in 2012. Gold bullion exports fell by 8 percent to $19.3 billion. The United Kingdom, Hong Kong, and Switzerland are regional centers for trading refined gold and were the destinations for 86 percent of U.S. exports of gold bullion. Exports of gold scrap declined by 72 percent to $2.3 billion, while exports of silver scrap fell by 40 percent to $2.1 billion in 2012. The decline in U.S. exports of gold scrap reflects both a quantity decrease of 397 metric tons (60 percent) and a unit-value decrease, due to a lower gold content in the scrap exported during 2012. Gold scrap inventories were drawn down in 2011 as a result of high U.S. secondary refinery output. The 2011 drawdown reduced the availability of gold scrap in 2012, depressing U.S. secondary refinery output and decreasing exports. Canada was the largest destination for U.S. exports of gold waste and scrap in 2012, accounting for 55 percent of exports or $1.3 billion.

Export reductions of iron and steel scrap, which fell by $1.9 billion (17 percent), also contributed to overall export declines within the minerals and metals sector. Turkey remained the largest destination for U.S. exports of iron and steel scrap in 2012, while there was a drop in U.S. exports to several other leading markets, including China, Taiwan, and the Republic of Korea (Korea). Overall, the drop in exports of iron and steel scrap may be attributed to robust demand for scrap in the United States, as steel production by the electric furnace method, which is the main use of such scrap, continued strong while scrap generation lagged.

These reductions in U.S. exports of minerals and metals were offset by the unrefined and refined gold subgroup, exports of which grew by $9.2 billion in 2012. Gold doré (a semi-pure alloy of gold and other metals, usually silver) accounted for the largest increase among all forms of unrefined and refined gold exports. U.S. primary refinery output of gold was relatively unchanged, indicating that consumption of unrefined gold by those refineries was similarly unchanged. U.S. mine output declined. Accordingly, exports of gold doré increased in parallel with a drawdown of domestic inventories. This export increase was partially offset by an increase in the volume of imports of gold doré. The increase was augmented by higher prices of gold in 2012, which were more than $97 per troy ounce above the previous year’s average of $1,572 per troy ounce. Switzerland, a global center for the refining, fabricating, and trading of gold and other precious metals, was the primary destination for U.S. exports, accounting for 80 percent of all U.S. exports of gold doré and for $8.3 billion (or 78 percent) of the U.S. export increase for gold doré in 2012. India became a significant destination for U.S. exports of gold doré for the first time, accounting for $1.6 billion in exports, compared to zero or insignificant amounts during prior years. The increase in exports of gold doré accounted for most of the overall increase in exports of minerals and metals to India.

U.S. Imports

The expansion of U.S. imports of minerals and metals was primarily driven by increased imports of steel mill products, unrefined and refined gold, and miscellaneous base metal products during 2012. However, reduced imports of natural and synthetic gemstones, in particular, offset these import gains. Imports of steel mill products rose by $3.5 billion (11 percent) to $34.3 billion in 2012. Within that category, imports of steel pipes and tubes of carbon and alloy steels rose by $2.7 billion (26 percent) to $11.3 billion. These import increases were driven by robust domestic demand for steel tubular products for use in oil and gas production and transportation projects.

U.S. imports of unrefined and refined gold registered the second-largest increase, growing by $1.6 billion to $15.9 billion in 2012. Unrefined gold doré accounted for the largest absolute increase in imports (rising $3.1 billion, or 41 percent, to $10.8 billion) among all forms of unrefined and refined gold, while imports of gold scrap increased by $0.6 billion (70 percent) to $1.6 billion. The top sources of gold doré were Mexico, Colombia, Peru, and Bolivia, all of which have major precious-metal mining industries. These countries accounted for $2.1 billion (67 percent) of the increase in imports of gold doré. The increase in imports of unrefined gold partially offset the even larger increase in U.S. exports mentioned above and was similarly augmented by higher gold prices during 2012.

U.S. imports of miscellaneous products of base metal registered the third-largest increase, as imports rose by $1.3 billion (10 percent) to $14.9 billion in 2012. Products within this subgroup include mountings, fittings, and similar articles for use in the production of motor vehicles. In 2012, the U.S. motor vehicle industry increased production to meet rising domestic and global demand, which likely translated into heightened demand for critical inputs, such as those found within the miscellaneous products of base metal subgroup. China, Mexico, and Canada were the top sources for $10.1 billion (or 68 percent) of all U.S. imports of these goods in 2012, which likely reflects each of these countries’ significance as leading suppliers of automotive parts to the United States.

Increases in U.S. imports of steel mill products and unrefined and refined gold were partially offset by a $2.0 billion reduction in U.S. imports of natural and synthetic gemstones in 2012. The United States is one of the world’s largest diamond markets but lacks notable diamond-bearing deposits, leaving the country highly dependent upon imports to meet domestic demand. Israel (Tel Aviv), India (Surat), and Belgium (Antwerp), all major diamond-processing locations (cutting and polishing) and trading centers, together accounted for $17.1 billion (or 87 percent) of U.S. imports of loose, worked diamonds in 2012. Such imports dropped nearly 10 percent by value in 2012, which was reportedly a “turbulent” year for the global diamond industry. During 2012, prices for 1-carat (0.2 gram) polished diamonds fell by 12.5 percent; disappointing holiday sales in the United States were attributed to economic uncertainties that dampened consumer confidence, depressing sales of diamond jewelry and other luxury goods.